Is Life Insurance Taxable in Canada?

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Is Life Insurance Taxable in Canada?

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Life insurance in Canada is often described as tax free, but that is only partly true. Whether tax applies depends on how and when the money is paid, and who receives it.

The confusion comes from the fact that different parts of a policy are treated differently. A death benefit, cash withdrawal, surrender value, or employer paid policy can each have different tax outcomes. Some may be tax free, while others can create a taxable event.

The better question is not whether life insurance is taxable. It is which part of the policy is involved and under what circumstances the money is paid.

At a Glance: Life Insurance Tax in Canada

- Death benefits paid to a named beneficiary are usually tax-free

- Cash surrender value may create taxable income if there is a gain

- Policy withdrawals can trigger tax depending on the amount taken

- Employer-paid group life insurance premiums may be a taxable benefit

- Interest earned after a payout is generally taxable

- Corporate-owned policies follow a different set of tax rules

- Most tax issues arise when the policy is used during life rather than paid at death

When Life Insurance Becomes Taxable

Life insurance typically becomes taxable when it begins to function as a financial asset rather than only as protection for beneficiaries. In most cases, that means the policy is being accessed during the policyholder’s lifetime rather than simply paying out at death.

Common situations where tax may apply include:

- Surrendering a policy and receiving its cash value

- Withdrawing money from a permanent policy

- Transferring ownership of the policy

- Borrowing against the policy and allowing it to lapse

- Receiving interest on proceeds before they are distributed

In these situations, the taxable amount is generally not the full amount received. Tax usually applies only to the gain or growth above the policy’s cost base. That distinction matters because it changes how much income is actually exposed to tax.

Is Cash Surrender Value of Life Insurance Taxable in Canada?

Permanent life insurance policies may build cash value over time. This value can grow within the policy, and that growth is not usually taxed immediately while it remains inside the contract. The tax issue arises when money is taken out.

If a policy is surrendered, part of the amount received may be taxable. In simple terms, the portion tied to the policy’s adjusted cost base is not usually taxed, but any amount above that can be treated as taxable income. This is one of the most common situations where life insurance creates an unexpected tax consequence.

That is why permanent policies should not be viewed only as tax-free tools. They can be tax-efficient, but once the cash value is accessed, the transaction needs to be understood more carefully.

Are Life Insurance Benefits Taxable in Canada?

Life insurance benefits are not taxable when they are paid directly to a named beneficiary. That remains the general rule and is the basis for how life insurance is commonly understood.

However, some related amounts can still create tax issues. The base death benefit may remain tax-free, while additional amounts tied to the payout are treated differently. This often happens when the funds are delayed, held, or earn interest after the death benefit becomes payable.

Situations where tax may apply include:

- Interest earned on the payout

- Funds left on deposit with the insurer

- Benefits paid into the estate rather than directly to a beneficiary

- Certain corporate or trust-related structures depending on ownership

The key point is that the insurance benefit itself is usually tax-free, but money earned around the payout may not be.

Group Term Life Insurance Taxable Benefit

Group term life insurance through an employer is often misunderstood because it involves two separate tax questions. The premium paid by the employer can be taxable to the employee, even though the death benefit itself is usually still paid tax-free to the beneficiary.

When an employer pays for group term life insurance, the value of that premium is often treated as a taxable benefit and included on the employee’s T4. That means the employee may pay tax on the value of the coverage while they are alive and employed.

This surprises many people because they assume that if the death benefit is tax-free, the premium must also be tax-free. In practice, those two parts are treated differently. The premium can create a taxable employment benefit, while the death benefit still passes to the beneficiary without income tax in most cases.

Where Tax Confusion Usually Happens

Most confusion around life insurance taxation does not come from obscure tax rules. It comes from combining different parts of the policy and assuming they all follow the same treatment.

Some of the most common misunderstandings include:

- Assuming all life insurance proceeds are always tax-free

- Assuming policy withdrawals do not create taxable income

- Assuming employer-paid coverage has no tax implications

- Assuming cash value can be accessed without consequence

- Assuming estate payout works the same as direct beneficiary payout

In reality, each part of the policy may be taxed differently depending on what is happening and when.

Get a quote to review how life insurance fits into your financial and tax situation.

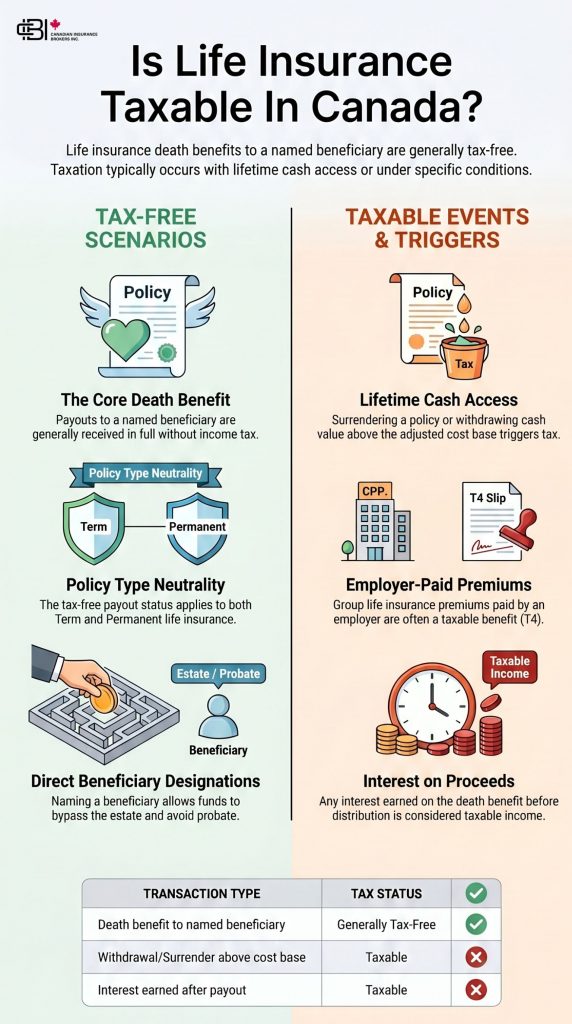

How Life Insurance Tax Treatment Can Differ

Different life insurance situations can lead to different tax outcomes. This visual gives a simple comparison of where tax concerns are more likely to arise.

General takeaway

Life insurance death benefits are often treated more favourably than policy withdrawals, surrenders, or interest-based payments. Once cash value is accessed or income is generated around the policy, tax treatment can become more complex.

Illustrative only. Actual tax treatment depends on policy design, adjusted cost basis, beneficiary setup, ownership structure, and how funds are withdrawn or paid.

The Role of Adjusted Cost Base (ACB)

One of the most important concepts in life insurance taxation is the adjusted cost base, or ACB. This is the figure used to help determine how much of a policy-related amount can be received tax-free and how much may be taxable.

Over time, the ACB changes based on how the policy is structured and how it has been funded. When money is withdrawn, when a policy is surrendered, or when certain ownership changes take place, the ACB helps determine whether there is a taxable gain.

A simple way to think about it is this:

- Amount up to the adjusted cost base is generally not taxed

- Amount above the adjusted cost base may be taxable

- The calculation matters most when the policy is accessed during life

This is one of the reasons people often benefit from advice before making changes to a permanent policy. A transaction that seems straightforward can have tax implications that are not immediately obvious.

Visual: Is Life Insurance in Canada Taxable?

What These Situations Look Like in Practice

Most life insurance tax issues follow the same general pattern. A policy is assumed to be fully tax-free, then at some point money is accessed, redirected, or handled in a different way. From there, the tax outcome depends on the nature of that transaction rather than the label attached to the policy.

A few simple examples make this easier to understand:

- A beneficiary receives a death benefit directly: usually no income tax

- A policyholder withdraws money from a permanent policy: possible taxable income

- A death benefit is delayed and earns interest: interest portion may be taxable

- An employer pays group premiums: taxable benefit may appear on the employee’s T4

The difference is not the existence of the policy itself. It is how the money moves and what type of value is being created.

If you’re also thinking about whether life insurance makes sense for you overall, read our blog on is life insurance worth it?

Get a quote to review your options and choose a structure that aligns with your situation.

How Life Insurance Fits Into Estate Planning

Life insurance is commonly used in estate planning because it can transfer value efficiently when structured properly. When a beneficiary is clearly named, the death benefit often passes directly to that person and generally avoids being treated as taxable income.

This can also help reduce delays and, in some cases, avoid probate-related complications that may apply when funds flow through the estate. That is one reason beneficiary designation matters so much. A policy that seems simple on paper can behave very differently depending on whether the proceeds are directed to an individual or to the estate.

When structured properly, life insurance can support estate planning by:

- Passing funds directly to named beneficiaries

- Avoiding unnecessary delay in the transfer of money

- Preserving the tax-free nature of the death benefit

- Supporting liquidity needs at death without triggering income tax on the benefit itself

Why Work With James Inwood

viewed through real-life decisions. This includes who owns the policy, who benefits, whether it has cash value, and how it fits into long-term planning.

James Inwood works with clients across Ontario to explain how life insurance works beyond the idea of being tax free. This includes reviewing beneficiary designations, cash value, employer coverage, and how different policy structures can affect outcomes over time.

Get a quote or book a call with James Inwood to review your life insurance.

Frequently Asked Questions

In most situations, beneficiaries do not need to report a life insurance payout as income on their tax return. The amount they receive is generally separate from regular taxable income like salary or investment earnings. However, if the funds are held and generate interest after the payout, that additional income may need to be reported. The key distinction is between the original benefit and anything earned afterward.

When a life insurance policy is paid into an estate rather than directly to a named beneficiary, the process can become more complex. The funds may be subject to probate, and delays can occur before the money is distributed. While the death benefit itself is still typically not taxed as income, the way it flows through the estate can create administrative costs and timing issues. This is why beneficiary designations are often reviewed carefully during planning.

Borrowing against a life insurance policy does not always create immediate tax, but it can lead to tax consequences depending on how the policy performs over time. If the loan grows and the policy lapses or is cancelled, part of the borrowed amount may be treated as taxable income. This situation is not always obvious at the time the loan is taken. It becomes relevant later if the structure of the policy changes.

Life insurance itself does not usually increase income tax directly, but it can interact with other financial elements. For example, employer-paid coverage may affect taxable employment income, and large payouts could influence estate-related planning decisions. In some cases, how a policy is structured can also affect how assets are transferred or reported. The impact is often indirect rather than a simple tax charge on the policy.

James Inwood is an Ontario-based insurance broker who works with individuals and families navigating life insurance and financial protection strategies. He focuses on helping clients understand how insurance works in real situations, including tax implications, policy structure, and long-term planning decisions.

His approach is practical and advisory, helping clients avoid common misunderstandings before they become financial issues.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn