Recruitment and Staffing Agency Insurance in Oakville, Ontario

Serving firms across Oakville, Halton Region, Burlington, Milton, Hamilton, Toronto & more

Recruiters and staffing agencies work under deadlines, handle sensitive candidate data, and make decisions that affect careers and business operations. When a placement fails, a credential is questioned, or a client alleges the process did not follow instructions, the dispute often turns into a claim about the services provided, the screening process, or the contract terms.

James Inwood arranges insurance for agencies, executive search firms, recruiters, temporary help agencies, HR professionals, and compliance advisors based in Oakville and throughout Ontario. Coverage is structured around real client requirements, clean certificates of insurance, and the specific work the firm performs.

Quick Glance: Recruitment and Staffing Agency Insurance

- Designed for recruitment firms, staffing agencies, executive search, and HR professionals

- Centres on Recruitment & Staffing E&O (professional liability) as the foundation

- Often paired with Commercial General Liability (CGL) and Cyber liability

- Can include Employers liability and Non-owned automobile liability when contracts require them

- Works for solo recruiters, incorporated agencies, and firms using contractors

What Is Recruitment & Staffing Agency Insurance?

Recruitment and staffing agency insurance is a combination of liability coverages that helps protect a firm when a client, candidate, or third party alleges the firm’s services caused financial loss or legal harm.

The core coverage is recruitment & staffing E&O, also known as professional liability insurance (some clients call it professional indemnity). It responds when a client claims the recruiting or staffing service failed to meet a professional standard, involved an error or omission, or resulted in a financial loss.

Because recruitment and staffing work is contract-driven, this insurance is often requested before vendor onboarding is approved, especially for enterprise accounts, public-sector buyers, and U.S. clients.

Who This Insurance Is For

This insurance is commonly set up for:

- Recruiters and recruitment agencies

- Staffing agencies and temporary help agencies

- Executive search firms and head hunters

- Contingency employment agencies and traditional employment agencies

- HR professionals and HR service firms

- Compliance advisors supporting hiring and workplace policies

- Meeting planners and event staffing coordinators placing workers for events

It can be arranged for:

- Self-employed and solo recruiters

- Sole proprietors

- Incorporated agencies

- Firms using contract recruiters or subcontractors

- Businesses with employees, temps, or interns

What Clients and Contracts Usually Require

Most client contracts and vendor portals ask for:

- Professional liability (E&O) with $1M or $2M limits

- Certificates of insurance (COIs) issued to the correct legal name

- Commercial General Liability (CGL) with specified limits

- Contract wording such as:

- Additional insured (usually on CGL)

- Waiver of subrogation

- 30 days’ notice of cancellation

- Confirmation that subcontractor work is addressed

Municipalities and public-sector clients often publish guidance outlining insurance expectations for professional service providers. This is an example of Mississauga professional and cyber liability requirements and certificate standards for vendors performing professional services.

Core Coverages for Recruitment, Staffing, and HR Firms

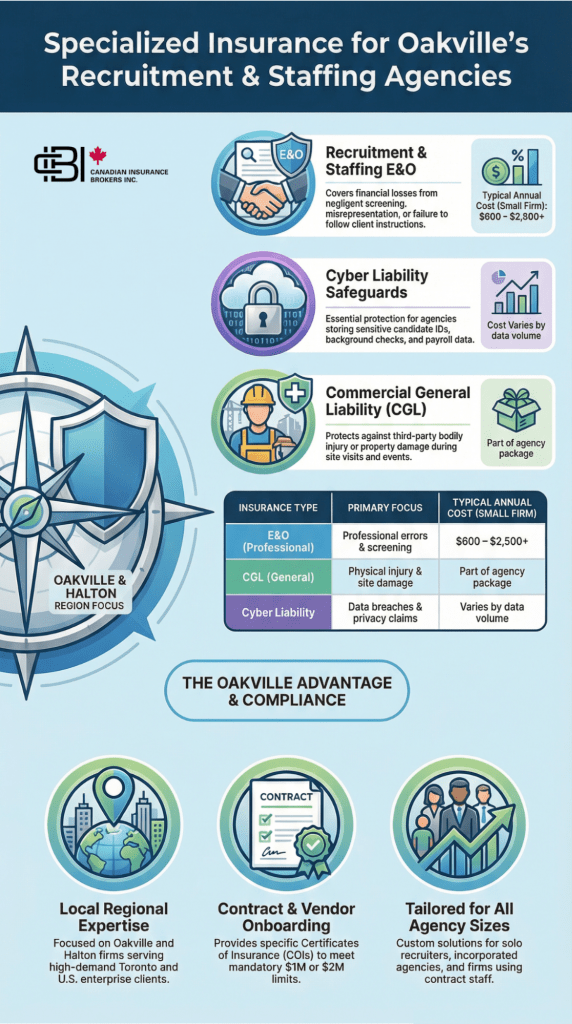

Recruitment & Staffing E&O (Professional Liability)

Helps respond when a client alleges the recruiting or staffing service caused financial loss. Common allegations include:

- Misrepresentation about credentials, experience, or licensing

- Negligent screening, reference checks, or verification

- Failure to follow client instructions or role requirements

- Disputes over placement guarantees, replacement obligations, or fees

- Confidentiality issues tied to candidate or client information

Commercial General Liability (CGL)

Covers third-party bodily injury and property damage. This is relevant when:

- Staff are present at a client site

- The agency attends job fairs, interviews, or events

- A third party alleges an on-site incident or damage

Cyber liability

Recruiters store resumes, IDs, background check details, and sometimes banking or payroll information. Cyber coverage can help with:

- Forensic investigation and breach response

- Notification and credit monitoring costs where required

- Legal support and privacy claims

- Extortion and ransomware response (where covered)

Employers liability

Relevant when there are employees, interns, temps, or ongoing contractors. Some insurers package this differently depending on the business setup and underwriting.

Non-owned automobile liability

Helps when the business is named in a lawsuit involving a vehicle it does not own, such as an employee using a personal vehicle for business errands or client visits.

Where Claims Usually Start

Most disputes start as routine issues and then escalate after a failed placement, a termination, a contract disagreement, or a data incident.

| Work activity | What goes wrong | How it becomes a claim |

|---|---|---|

| Screening and referrals | Credentials, experience, or licensing are disputed | Client alleges negligent referral or misrepresentation |

| Placement terms and guarantees | Fee, guarantee, or replacement language is challenged | Breach of contract demand and legal defence |

| Handling candidate information | Data is shared without consent, exposed, or accessed improperly | Privacy complaints, response costs, and lawsuits |

| On-site staffing and events | Incident at a client location (injury or property damage) | CGL claim and defence costs |

Real Claim Examples Involving Recruitment and Staffing Agencies

Example: A Canadian HR report noted that poor hiring practices are contributing to talent shortages, raising questions about recruitment and screening decisions.

How insurance helps: Recruitment & staffing E&O can help respond if a client alleges hiring or screening decisions caused financial loss, subject to policy terms.

Example: The Government of Canada described a security incident involving a third-party multi-factor authentication service provider that exposed certain contact details and led to phishing messages.

How insurance helps: Cyber liability can help with incident response costs and legal support if a firm is drawn into a dispute about security controls, depending on policy wording.

Example: A reported lawsuit involving an HR specialist highlighted how workplace conduct allegations and internal handling can end up in litigation.

How insurance helps: Employers-related coverage and, in some cases, professional liability can help respond to defence costs, subject to the policy and the allegations.

Coverage Comparison: E&O vs CGL vs Cyber

- E&O (Professional Liability): Claims about recruiting services, screening, placement process, misrepresentation, and contract performance

- CGL: Bodily injury or property damage arising from operations or on-site activities

- Cyber Liability: Breaches, ransomware, privacy claims, and breach response costs

Many recruitment firms carry E&O + CGL, then add cyber when they store large volumes of candidate data or work with enterprise clients.

Service Areas in Ontario

James Inwood works with recruitment and staffing firms in:

- Oakville

- Mississauga

- Burlington

- Milton (including Campbellville)

- Georgetown

- Halton Hills (including Acton)

- Hamilton

- Toronto

- And, more!

Oakville and Halton have a high concentration of professional service businesses, including recruitment firms, staffing agencies, and HR specialists. Many local agencies support Toronto clients or U.S. companies where proof of E&O, cyber coverage, and clean certificates is required before work begins. Contracts often spell out minimum limits, certificate wording, and insurance clauses tied to hiring, placement, and HR services.

Client Requirement Checklist

Before signing a new agreement, this checklist helps avoid certificate delays:

- Named insured matches the legal business name

- E&O limits meet contract requirements ($1M or $2M)

- CGL included with correct limit

- Additional insured wording confirmed (CGL)

- Non-owned auto included if requested

- Cyber included if required by vendor onboarding

- Certificate wording matches contract language

- Subcontractor work is addressed

How Much Does Recruitment and HR Professional Insurance Cost in Ontario?

Cost depends on services (executive search vs temp staffing), revenue, contract requirements, and data handling.

Common ranges seen for smaller firms:

- Solo recruiter / small HR professionals: often $600 to $2,500 per year for core E&O

- Small staffing agency: often $1,500 to $5,000+ per year once E&O, CGL, and cyber are combined

Higher limits, U.S. contracts, temp staffing exposures, and cyber limits can increase premiums.

How To Get Recruitment & Staffing Agency Insurance

- Describe the services: Recruitment only, executive search, temp staffing, compliance work, or event staffing.

- Share the contract: James Inwood reviews the insurance section and matches coverage and wording to the agreement.

- Issue certificates that pass onboarding: Coverage is issued in the correct legal name and certificates are prepared to match the client’s requirements.

Visual: Specialized Insurance for Oakville’s Recruitment & Staffing Agencies

Why Recruitment & Staffing Firms Choose James Inwood

James Inwood is a licensed Ontario insurance broker based in Oakville. Clients work with James because he understands how recruitment, staffing, and HR service contracts are written, and what insurers look for when underwriting professional liability (E&O), CGL, and cyber coverage.

Many firms in Oakville and the Halton Region support clients across the GTA and the U.S. James helps them meet contract insurance requirements, issue certificates correctly, and avoid gaps between what a contract demands and what a policy actually covers.

Get a quote or talk to James to review your services, contracts, and coverage needs.

Frequently Asked Questions

Not by itself. E&O is for claims that your process or service caused financial loss, like alleged misrepresentation, missed screening steps, or not following written instructions.

That can trigger a claim about confidentiality or privacy. Depending on how it’s alleged, it may involve E&O (professional services) and sometimes cyber/privacy coverage.

Often, yes. E&O covers disputes about the placement or recruiting service. CGL covers bodily injury or property damage, which matters when workers are on client sites or at events.

Sometimes, but not always. Coverage depends on whether contractors are included in the policy wording and how they are engaged. This is worth checking before relying on it.

Sometimes, but it has to be set up that way. Territory, jurisdiction, and contract wording can change what insurers will offer.

James Inwood

James Inwood is a licensed Ontario insurance broker who works with recruitment agencies, staffing firms, and HR consultants across Oakville and surrounding areas. He focuses on professional liability, recruitment & staffing E&O, cyber coverage, and contract-driven insurance requirements.