Joint Life Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Joint Life Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Joint life insurance is often introduced as a straightforward way for couples to combine coverage under one policy. In reality, the structure behind it plays a much bigger role than most people expect. The way the policy is set up determines when it pays out, who benefits, and whether it continues to meet financial needs over time.

For many households in Ontario, the decision comes up during practical moments. Buying a home in Toronto, taking on a larger mortgage in Oakville, raising a family in Burlington, or planning long term in Ottawa or London naturally leads to the question of how to protect a shared financial structure. At that point, joint coverage can seem like the most efficient option.

The important part is understanding what that efficiency actually means in practice. A joint policy simplifies things at the start, but it can also introduce limitations that are not always obvious until later.

At a Glance: Joint Life Insurance

Joint life insurance brings two people under one policy, with a single payout triggered by how the policy is structured.

- One policy covering two individuals

- A single benefit paid either on the first or second death

- Commonly used by couples or business partners

- Simpler to manage than separate policies

- Less flexible once in place

Why Joint Coverage Comes Up in Real Situations

Joint life insurance is rarely a starting point on its own. It usually comes up when financial responsibilities are already shared. That could mean a mortgage, ongoing living expenses, or long-term planning tied to two people rather than one.

This is especially common in places where housing costs create larger shared obligations. In Toronto, Mississauga, and Oakville, for example, couples are more likely to be carrying larger mortgage balances, which makes the question of life insurance feel less theoretical and more practical. In cities like Hamilton, Kitchener, Waterloo, and London, the conversation may center more around income replacement and family stability than just debt protection.

In those situations, the real goal is not simply to have coverage. It is to protect the structure that two people have built together.

Get a quote to compare joint life insurance options based on your situation.

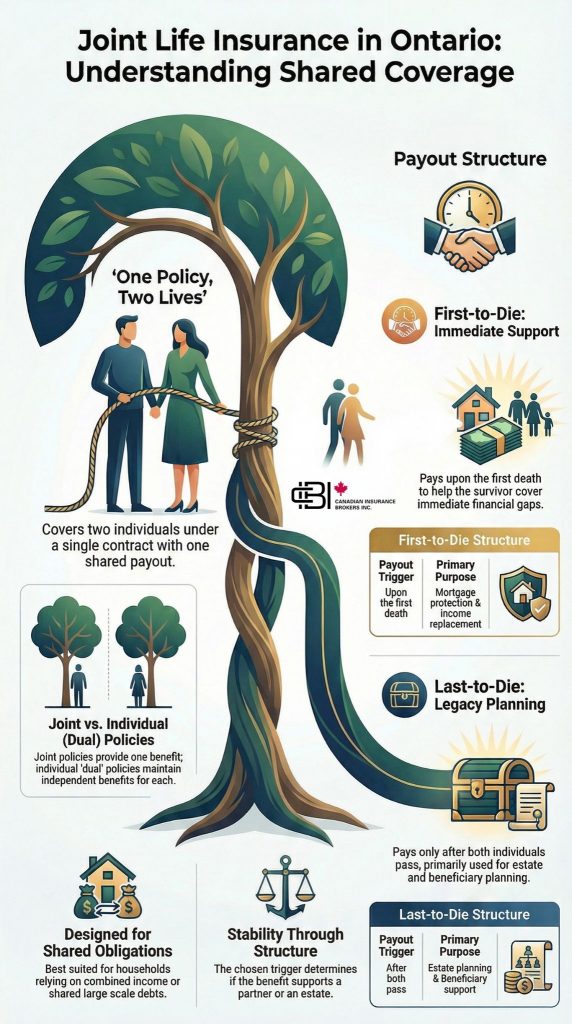

How the Policy Pays Out and Why It Matters

The defining feature of joint life insurance is how the payout is triggered. There are two common structures, and each one serves a different purpose depending on the situation.

A first-to-die policy pays out when one person passes away. This is typically used to support the surviving partner by helping cover immediate financial obligations. It is designed for situations where the loss of one income would create an immediate gap.

A last-to-die policy delays the payout until both individuals have passed away. This shifts the purpose toward estate planning, where the benefit is intended for beneficiaries rather than for ongoing financial support.

The structure is what determines the outcome. Choosing the right one depends on when that financial support is actually needed.

Where Joint Life Insurance Fits Naturally

Joint life insurance is most effective when financial responsibilities are shared. In these situations, the policy aligns with how a household or partnership already functions day to day. It’s commonly considered for:

- Shared mortgages or significant financial commitments

- Households that depend on combined income

- Long-term estate planning needs

- Business partnerships with joint financial risk

The way this plays out can vary by location. For example, in Ontario, it often focuses on protecting larger mortgages or managing a higher cost of living. Ultimately, joint life insurance works best when the coverage mirrors how financial risk is actually shared.

Joint Life vs Dual Life Insurance

Joint life insurance is sometimes confused with what people refer to as dual life insurance, but the difference comes down to how the coverage is structured.

A joint policy insures two people under one contract and provides a single payout. Dual life insurance, on the other hand, typically refers to two separate individual policies held by each person. While the wording sounds similar, the way the coverage works is very different.

With dual coverage, each person maintains their own policy and their own benefit. That means coverage continues independently, even after one payout. A joint policy does not work that way, since it is built around a single shared outcome.

In practical terms, dual life insurance is simply another way of describing individual coverage. The real decision is whether to combine coverage into one policy or keep it separate.

How Joint Life Insurance Structures Compare

| Coverage Type | How It Works | When It Pays Out | Best Fit For |

|---|---|---|---|

| Joint First-to-Die | One policy covering two people with a single payout | After the first insured person passes away | Couples with shared debts, mortgage obligations, or income dependence |

| Joint Last-to-Die | One policy covering two people with one payout at the end of both lives | After both insured people have passed away | Estate planning, wealth transfer, and legacy-focused planning |

| Dual Life / Separate Policies | Two individual policies, each with its own benefit | Each policy pays independently when that insured person passes away | Couples who want flexibility, separate coverage needs, or long-term independence |

Why Simplicity Can Become a Limitation Later

Joint life insurance is often chosen because it feels simple at the beginning. One policy, one premium, and one shared structure can be appealing, especially when life is already busy.

But simplicity at the beginning does not always translate into flexibility later. Over time, relationships evolve, financial responsibilities shift, and future plans can change. A policy that felt efficient at the start may feel restrictive later if one person’s needs change more than the other’s.

This matters in all parts of Ontario, but it tends to become especially noticeable in cities where households are under more financial pressure. In places like Toronto, Mississauga, and Oakville, where larger mortgages and higher monthly costs already create stress, a policy that no longer fits well can become more problematic.

That does not make joint coverage a poor choice. It simply means it works best when stability is expected and when the structure has been chosen carefully from the start.

How to Decide If Joint Life Insurance Is Right for You

One of the most useful ways to approach joint life insurance is to step away from the product itself and focus on the situation it’s meant to support. The question is not simply whether joint coverage is available, but whether it matches how financial responsibility is shared between two people.

In most cases, the decision becomes clearer by looking at a few practical factors:

- Whether both partners contribute equally to major expenses

- Whether one person depends financially on the other

- Whether the goal is short-term protection or long-term estate planning

- Whether flexibility will be important later

If the financial structure is tightly connected and unlikely to change, a joint policy can work well. If there is uncertainty or a need for independence in coverage, separate policies often provide more control. The right decision comes from aligning coverage with how real financial risk exists, not just how it appears on paper.

Common Mistakes People Make With Joint Life Insurance

Joint life insurance is often chosen quickly because it feels straightforward, but that simplicity can lead to decisions that are not fully thought through. Many of the issues people run into later are not due to the product itself, but how it was selected. Some of the most common mistakes include:

- Choosing a first-to-die policy when long-term coverage is still needed

- Focusing only on cost instead of structure

- Assuming the policy works like two individual policies combined

- Not considering how the policy would work after a major life change

- Overlooking how ownership and control of the policy is set up

These are not obvious issues at the beginning, which is why they tend to surface later. Taking the time to understand how the policy behaves in different scenarios can prevent gaps that only become visible after the fact.

Looking Beyond Cost When Comparing Options

Joint life insurance can be less expensive upfront, but that does not always mean it is the better long-term option.

Typical Ontario ranges:

- Joint first-to-die policy for a couple in their 30s: $30 to $60 per month

- Two separate individual policies combined: $50 to $90 per month

The price difference may matter more in some cities than others. In Toronto, Oakville, and Mississauga, where household budgets are often already stretched by housing costs, the appeal of a lower monthly premium can be strong. In cities like Hamilton, London, or Kingston, the pressure may be slightly lower, but the same question still applies.

The real comparison is not just what the policy costs today. It is how the policy performs if life changes, if one person dies, or if the need for flexibility becomes more important later.

Choosing a Structure That Actually Fits

The most effective way to approach joint life insurance is to focus on what the coverage is meant to achieve. That means thinking about when the payout would be needed, who depends on it, and how long coverage should remain in place.

A clear review usually involves:

- Identifying shared financial responsibilities

- Understanding when financial support would be required

- Considering how flexible the policy needs to be

- Comparing joint and separate structures side by side

Get a quote to review your options and choose a structure that aligns with your financial situation.

Why This Decision Matters Over Time

Life insurance decisions are often made once and left unchanged for years. Joint life insurance adds another layer to that because it connects two people within a single structure.

If the policy aligns with both current and future needs, it can work well. If it does not, the limitations often become more noticeable later. That is why this decision benefits from being looked at carefully from the start rather than adjusted after the fact.

In cities with higher household costs, such as Toronto, Oakville, or Mississauga, the consequences of getting that structure wrong can be more pronounced because the financial obligations being protected are often larger.

Visual: Joint Life Insurance in Ontario

Why Work With James Inwood

James Inwood works with individuals and families across Ontario who want a clearer understanding of how life insurance performs in real situations. Joint life insurance is often presented as a simple option, but the differences between structures are not always obvious until they are explained properly.

His approach focuses on helping clients compare options clearly, understand how each structure works over time, and choose coverage that reflects how their financial situation is actually set up. By working with multiple insurers, he provides perspective beyond just the initial purchase.

Get a quote or book a quick call with James Inwood to compare joint life insurance and separate coverage options.

Frequently Asked Questions

Yes. As long as there is a shared financial interest, joint life insurance can be used by common-law partners or unmarried couples.

In most cases, no. The policy typically ends after the benefit is paid, depending on how it is structured.

Not necessarily. Pricing depends on both individuals and the type of policy, so the difference is not always significant.

Changes can be more limited compared to individual policies, which is why structure should be considered carefully upfront.

James Inwood is an Oakville-based insurance advisor who works with individuals, families, and business owners across Ontario, including Toronto, Burlington, Mississauga, and surrounding communities. He focuses on helping clients understand how insurance performs in real-world situations, including life insurance structure, coverage decisions, and long-term planning.

His approach is grounded in practical guidance, with a focus on aligning policies with how people actually live, borrow, and plan financially.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn