How Spring Construction Can Affect Your Home and Auto Insurance in Oakville

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

How Spring Construction Can Affect Your Home and Auto Insurance in Oakville

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Spring is one of the busiest construction seasons in Oakville. As weather improves, homeowners begin renovations, additions, demolitions, custom home projects, and property upgrades across Bronte, Glen Abbey, Kerr Village, Downtown Oakville, West Oakville, and Trafalgar.

What many homeowners do not realize is that construction can affect insurance before work begins. Changes to occupancy, demolition plans, vacancy periods, contractors, permits, and project timelines can all impact how coverage applies during the project.

For homeowners planning renovations or custom home construction, insurance should be reviewed early. The goal is to avoid gaps between a standard home policy, vacancy coverage, builders risk insurance, contractor liability, and the transition back to regular home insurance.

At a Glance: Spring Construction Insurance Risks

- Spring construction projects can affect home and auto insurance

- Demolition and vacancy can create insurance gaps

- Builders risk insurance may be needed for major renovations or rebuilds

- Occupancy status matters during construction

- Demolition permits and building permits can affect insurance planning

- Contractor activity increases liability exposure

- Insurance should be reviewed before work begins

Why Spring Construction Changes Insurance Risk

Construction changes how insurers view a property.

A standard homeowner policy is designed for an occupied home with normal residential use. Once demolition, structural renovations, excavation, or vacancy begin, the risk profile changes.

This can include:

- Increased fire exposure

- Water damage risk

- Theft of building materials

- Injury involving contractors or visitors

- Damage to neighbouring properties

- Vacant property exposure

- Heavy equipment on site

This is why insurance often needs to change during the construction process.

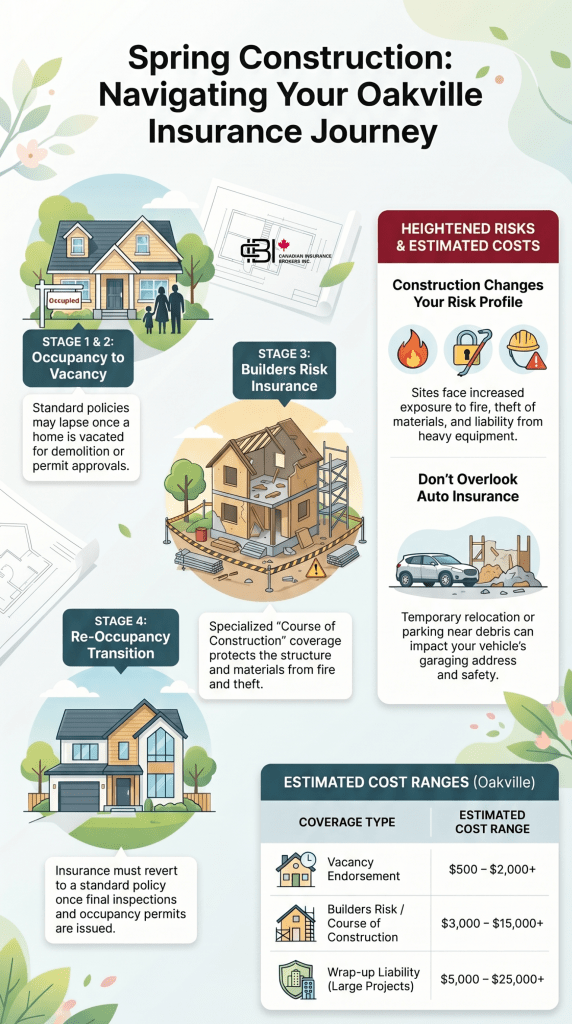

From Occupied Home to Active Construction Coverage

Many Oakville homeowners buy older homes with plans to renovate, demolish, or rebuild later. Insurance needs can change at each stage.

Stage 1: Standard Homeowner Insurance

Before construction starts, the home may still qualify for standard homeowner insurance if it is occupied normally.

However, insurers may ask questions about:

- Planned demolition

- Major renovations

- Vacancy periods

- Contractor activity

- Permit applications

Failing to disclose planned construction can create problems later if a claim occurs.

Stage 2: Vacancy Exposure

Once a property becomes vacant, insurance risk increases.

This often happens when:

- Homeowners move out before demolition

- The property is waiting for permits

- Renovations make the home temporarily unlivable

- The project is delayed between demolition and rebuilding

Vacant homes typically carry higher risks for vandalism, water damage, fire, break-ins, and undetected losses.

Some homeowner policies restrict or limit coverage after a property has been vacant for a certain period of time. This becomes especially important in Oakville neighbourhoods like Kerr Village or Downtown Oakville, where older homes are often purchased for redevelopment.

Stage 3: Builders Risk or Course of Construction Insurance

Once major construction begins, a standard home insurance policy may no longer provide the right protection.

Builders risk insurance is designed for homes that are being built, rebuilt, or significantly renovated. It can help protect the structure, materials, and overall project value while construction is underway.

You may also hear this coverage referred to as Course of Construction insurance. To understand how the terms are used and when they may differ, read our blog on the difference between COC and builders risk.

Stage 4: Occupancy and Home Insurance Transition

When construction is complete, insurance may need to transition again.

This usually involves:

- Final inspections

- Occupancy permit status

- Updated replacement cost

- Confirmation of completed work

- Transition from builders risk to homeowner insurance

Insurance should follow the project from planning to occupancy, not just the active construction stage.

Insurance Policies Affected by Spring Constructions

A spring renovation or rebuild can affect more than one policy. Home, vacancy, builders risk, contractor liability, and auto insurance may all need to be reviewed before work begins.

Home Insurance

Standard home coverage may change once the property is under renovation, vacant, or no longer used as a normal residence.

Vacancy Coverage

If the home is empty while waiting for permits, demolition, or construction, vacancy restrictions may apply.

Builders Risk

Major renovations, rebuilds, and custom home projects may need builders risk or Course of Construction coverage.

Contractor Liability

Contractors and trades should carry their own liability insurance, especially when demolition, excavation, or structural work is involved.

Auto Insurance

Temporary relocation, different overnight parking, or construction site exposure may affect how vehicles are insured.

This visual is for general planning only. Actual coverage depends on insurer rules, policy wording, project scope, and construction timeline.

What to Know Before Buying a Home You Plan to Demolish

Many redevelopment projects in Oakville begin with buying an older property that will later be demolished. Insurance should be reviewed before closing on the property, not after demolition planning begins.

Important considerations include:

- Whether the insurer knows about the demolition plans

- How long the property may remain vacant

- Whether demolition contractors carry proper insurance

- When builders risk coverage should begin

- Whether liability changes once demolition starts

- Permit timelines and construction delays

A home purchased only for redevelopment may not fit cleanly under a standard homeowner policy for very long.

How Spring Construction Can Affect Auto Insurance

Construction projects can also affect auto insurance in ways homeowners may overlook.

Examples include:

- Vehicles parked near active construction

- Nail, debris, or material damage near the property

- Increased traffic from contractors and deliveries

- Temporary relocation during renovation or rebuilding

- Changes in where vehicles are parked overnight

If homeowners temporarily move during construction, insurers may need an updated garaging address for vehicles.

Where Spring Construction Creates Insurance Gaps

Insurance gaps often appear when the property changes use, contractors enter the site, or construction timelines shift.

This visual is for general planning only. Actual risk and coverage depend on the insurer, policy wording, construction scope, and project timeline.

Real Construction Claim Example

Construction claims often become more complicated when projects involve vacancy, permits, demolition, and multiple contractors.

A construction-related legal case involved water escaping from a sprinkler system during a hospital renovation project. The flooding caused damage beyond the active construction area, leading to disputes over whether the loss should fall under builders risk insurance or contractor liability coverage.

These examples show why construction insurance is not only about physical damage to the structure itself. Claims can involve neighbouring properties, contractors, legal defense costs, water damage, and disputes between multiple insurers and project parties.

What Construction Insurance Can Cost in Oakville

Insurance costs vary depending on the project, insurer, and scope of work.

Approximate Oakville ranges may include:

- Vacancy endorsement or vacant property coverage: approximately $500 to $2,000+

- Builders risk or Course of Construction insurance: approximately $3,000 to $15,000+

- Wrap-up liability for larger projects: approximately $5,000 to $25,000+

Factors affecting cost include:

- Project value

- Demolition exposure

- Property location

- Construction timeline

- Vacancy duration

- Neighbouring property exposure

- Contractor activity

- Requested liability limits

Why Work With James Inwood

Construction insurance involves more than simply adding coverage to a homeowner policy. Demolition, vacancy, permits, builders risk insurance, contractor liability, and occupancy timing all affect how insurance applies during a project.

James Inwood works with homeowners, builders, and contractors in Oakville, including Bronte, Glen Abbey, Kerr Village, Downtown Oakville, West Oakville, and Trafalgar. He also serves clients across Ontario navigating construction and redevelopment projects.

Get a quote or book a meeting with James Inwood to review insurance options before your construction project begins.

Frequently Asked Questions

Not often. Once demolition begins, many standard homeowner policies may no longer provide appropriate coverage because the property risk changes significantly. Builders risk or specialized construction coverage may be needed.

This depends on the insurer and policy wording. Some policies apply restrictions after a property has been vacant for a certain number of days. Homeowners should notify their insurer before extended vacancy begins. Some policy can be insured as short as 4 days and range to 30 days.

Yes. Some contractors may ask who is responsible for insuring the project before starting work, especially on larger renovations, additions, or rebuilds. This helps clarify whether the homeowner, builder, or another party is arranging coverage for the structure and materials.

Yes. Permit delays can extend the vacancy or construction period, which may increase the cost of vacant property coverage or builders risk insurance. For example, if a project is delayed between demolition and rebuilding, the property may remain exposed for longer than originally expected.

Yes. Insurers may ask for details about the general contractor, subcontractors, project value, and type of work. Contractors should also carry their own liability coverage, even when builders risk or other project coverage is arranged.

James Inwood is an Ontario-based insurance broker who works with homeowners, contractors, and builders involved in renovations, custom homes, demolition, and construction projects. He helps clients understand how insurance applies throughout the construction process, including vacancy exposure, builders risk insurance, contractor liability, demolition planning, and occupancy transitions.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn