Water Damage Insurance and Coverage

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Water Damage Insurance and Coverage

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

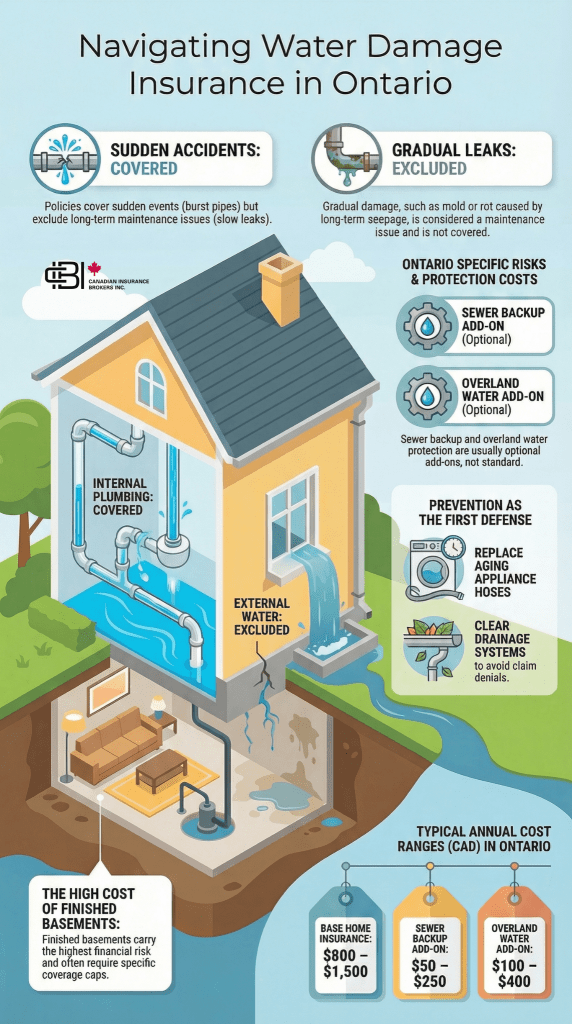

Water damage is one of the most common insurance claims in Canada, but it is also one of the most misunderstood. Many homeowners assume that if water damages the home, insurance will automatically respond.

A burst pipe, a slow leak behind a wall, and water entering through a basement after heavy rain may all look similar once the damage is visible. From an insurance standpoint, they are treated very differently. That difference often determines whether a claim is paid, limited, or denied.

In Ontario, this matters even more. Basement exposure, aging plumbing, and changing weather patterns all increase the likelihood of water-related loss, especially in urban areas like Toronto, Mississauga, and Hamilton where older infrastructure and higher density can amplify risk.

Understanding how coverage actually responds is what helps avoid expensive surprises.

At a Glance: Water Damage Insurance in Ontario

- Sudden and accidental damage is often covered

- Gradual or long-term damage is usually excluded

- Sewer backup and overland water often require added coverage

- Basement exposure significantly increases risk

- Coverage gaps are often discovered only during a claim

- Risk varies by city, especially across the GTA and older neighbourhoods

What Is Water Damage Insurance & What Does It Cover?

Water damage insurance is not a single type of protection. It is a combination of coverages within a home insurance policy, along with optional endorsements that expand what is included.

At its core, insurance is designed to respond to unexpected events. When water damage happens suddenly, such as from a pipe failure or appliance issue, the policy is more likely to respond.

Where things become less clear is when water damage develops over time or comes from outside the home. In those situations, coverage depends heavily on how the policy is structured.

Where Coverage Usually Holds Up

Most policies are built to respond to sudden internal water events that are clearly accidental.

Common examples include:

- Burst pipes during colder months

- Failed washing machine or dishwasher hoses

- Unexpected hot water tank leaks

These are situations where the cause is identifiable and immediate. That is the type of loss insurance is designed to handle.

The Line Between Covered and Uncovered Damage

One of the most important distinctions in water damage insurance is the difference between sudden and gradual loss. A sudden event, like a pipe bursting overnight, is typically treated very differently from a slow leak that has been developing for months. From an insurance perspective:

- Sudden damage is usually insurable

- Gradual damage is often considered maintenance

This is where many claims become complicated. By the time damage becomes visible, it may appear sudden, but the underlying cause may not be.

Where Most Coverage Gaps Actually Exist

Water damage exposure is not limited to what happens inside the home. Many of the biggest gaps appear where water enters from outside or below. Common risk areas include:

- Sewer backup into basements

- Water entering through foundation walls

- Heavy rainfall overwhelming drainage systems

- Groundwater or surface water intrusion

These scenarios are not always fully covered under a standard policy. In many cases, they depend on whether specific water endorsements have been added. For homeowners with finished basements, this is often the most important part of the entire policy.

For homeowners in areas like Toronto, Etobicoke, and older parts of Hamilton, where sewer systems and drainage infrastructure can be under pressure, this becomes particularly relevant.

How Water Damage Risk Changes by City

Water risk is not evenly distributed across Ontario. It varies based on infrastructure, geography, and housing type.

In practical terms:

- Toronto and Mississauga: Higher sewer backup and urban flooding exposure due to density and aging systems

- Brampton and Vaughan: Increased claim frequency tied to rapid development and stormwater pressure

- Oakville and Burlington: Moderate risk, but still exposed due to basement-heavy housing and storm events

- Hamilton and older cities: Higher likelihood of plumbing-related issues in aging homes

- Ottawa and Kingston: Seasonal risks tied to freezing and thaw cycles

This means two similar homes can have very different insurance outcomes based on location alone.

How Water Damage Coverage Is Structured in a Policy

Water coverage is not grouped into a single category within a policy. It is typically divided into multiple layers, each addressing a different type of risk.

For example, a policy may treat internal plumbing failures differently from sewer backup or external water intrusion. Each of these categories can have its own limits, deductibles, and conditions.

A policy might fully cover one type of water loss while limiting or excluding another. Understanding how these layers are built is what allows homeowners to identify where protection is strong and where it may fall short.

Policy Limits, Deductibles, and What Actually Gets Paid

Even when water damage is covered, the payout depends on how the policy is structured. Two key elements affect the outcome:

- Coverage limits: Some water-related losses have caps that are lower than the overall home value

- Deductibles: Water claims may carry different deductibles depending on the type of loss

For example, a home in Toronto with a finished basement may have high reconstruction costs, but still carry a capped sewer backup limit. That difference can significantly affect what is paid after a claim.

How Water Risk Changes by City in Ontario

Water damage risk is not uniform across Ontario. It changes based on geography, infrastructure, and property type.

In higher-density urban areas like Toronto and Mississauga, the main concern is often sewer backup and drainage capacity. In rapidly growing areas like Milton and Brampton, surface water and overland flooding have become more relevant due to development patterns.

In smaller cities like Kingston or Windsor, aging infrastructure and weather variability can create different types of exposure.

What this means in practice

- Toronto: Higher sewer backup and basement flooding risk

- Brampton / Mississauga: Increased overland water exposure

- Oakville / Burlington: Higher-value homes with finished basements increase claim size

- Ottawa / Barrie: Freeze-related pipe damage more common

This is why water coverage should be reviewed based on location, not just the home itself.

Reducing the Chance of a Claim

Insurance is only part of the solution. Prevention plays a major role in reducing risk. Simple steps include:

- Replacing aging hoses and plumbing connections

- Monitoring areas prone to moisture

- Keeping drainage systems clear

- Watching for early warning signs like staining or odours

In areas like the GTA, where claim frequency is higher, preventative maintenance can significantly reduce long-term risk.

Get a quote before a claim happens and make sure your policy includes the protection your home actually needs.

How Insurers Evaluate Water Risk

Insurance is priced and structured based on risk, and water exposure is one of the most closely evaluated areas. Insurers often consider:

- Age and condition of plumbing systems

- Previous water damage claims

- Presence of sump pumps or backwater valves

- Location-specific drainage or flooding exposure

- Whether the basement is finished

In cities like Toronto, Oakville, and Mississauga, these factors can significantly affect both pricing and eligibility.

Why Basement Risk Changes Everything

Basements tend to carry the highest exposure when it comes to water damage. This is where:

- Water is most likely to accumulate

- Damage can spread quickly across finished space

- Costly repairs are more likely

For homes with finished basements or secondary living spaces, even a small water event can lead to major financial loss.

In areas like Oakville and Burlington, where finished basements are common, this becomes one of the most important parts of the entire policy.

How Water Damage Coverage Usually Works in Ontario

| Water Source | Typical Coverage Position | Often Requires Add-On? | Main Consideration |

|---|---|---|---|

| Burst pipe | Often covered | No | Was the damage sudden? |

| Appliance failure | Often covered | No | Maintenance vs unexpected failure |

| Sewer backup | Often limited | Yes | Endorsement in place? |

| Overland flooding | Often excluded | Yes | Flood coverage added? |

| Slow leak | Often excluded | No | Gradual vs sudden damage |

Cost of Water Damage Insurance in Ontario

Water damage coverage is typically included as part of a home insurance policy, but the cost varies depending on location and risk.

Typical ranges:

- Base home insurance: $800 to $1,500 per year

- Sewer backup add-on: $50 to $250 per year

- Overland flood coverage: $100 to $400 per year

In higher-risk cities like Toronto or Brampton, premiums tend to sit at the higher end of these ranges. In areas like Ottawa or Kingston, they may fall slightly lower depending on exposure.

Strengthening Your Coverage Before It’s Needed

The most effective time to review water coverage is before a claim happens. A proper review usually includes:

- Confirming sewer backup coverage

- Checking for overland water protection

- Understanding any limits or sublimits

- Reviewing deductibles relative to risk

Small adjustments here can make a significant difference in how a policy responds.

Get a quote to review your home insurance and make sure your water coverage reflects your actual risk.

Visual: Navigating Water Damage Insurance in Ontario

Why Work With James Inwood

James Inwood works with homeowners across Ontario who want a clearer understanding of how their insurance performs in real situations.

Water damage is one of the most misunderstood areas of home insurance because the outcome often depends on details most people are not aware of until after a loss.

His approach focuses on identifying those details early, reviewing coverage structure, and making sure policies align with the actual risks a home faces.

Get a quote or book a quick call with James Inwood to make sure your coverage is built for how your home is actually used.

Frequently Asked Questions

Yes. Coverage depends on the cause and timing of the damage, not just how serious it appears.

No. Some types of water damage have separate limits or caps within the policy.

Yes. Finished basements increase potential damage and may require additional coverage.

No. Different sources of water are treated differently depending on the policy structure.

James Inwood is an Oakville-based insurance advisor who works with homeowners across Ontario. He focuses on helping clients understand how insurance performs in real-world situations, including water damage, claims, and coverage gaps.

His approach is grounded in practical guidance, with a focus on aligning policies with the risks a property actually faces.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn