What Is a Deductible in Car Insurance?

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

What Is a Deductible in Car Insurance?

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

A car insurance deductible is one of those policy details most drivers have seen, but not everyone fully understands. It is often mentioned when you buy coverage, but it usually becomes much more important when a claim actually happens.

In Ontario, your deductible affects both what you pay for insurance and what you could pay out of pocket if your vehicle is damaged. That makes it more than just a small line item on your policy. It is one of the key factors that shapes how your coverage works in real life.

Understanding deductibles can help you make better decisions about premium, risk, and the type of financial exposure you are comfortable with.

At a Glance: Car Insurance Deductibles

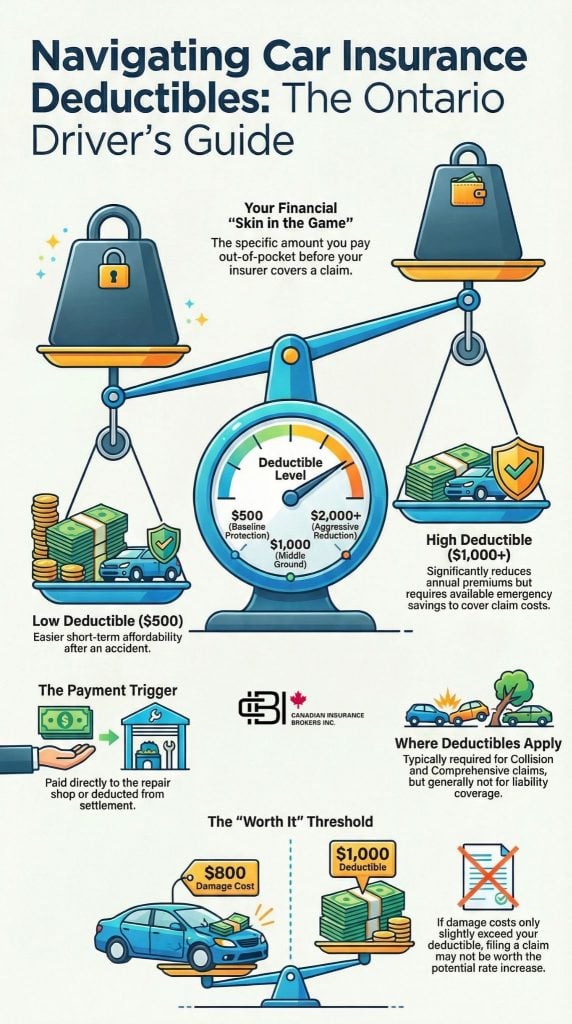

- A deductible is the amount you pay before insurance covers the rest of a claim

- It usually applies to collision and comprehensive coverage

- It generally does not apply to liability claims

- Higher deductibles usually lower your premium

- Lower deductibles usually increase your premium

- Many Ontario drivers choose deductibles between $500 and $1,000

What a Car Insurance Deductible Actually Means

A deductible is the portion of an insured loss that you agree to pay yourself before your insurer pays the remaining covered amount.

If your vehicle has $5,000 in covered damage and your deductible is $1,000, you would pay the first $1,000 and your insurer would cover the remaining $4,000.

From an insurance standpoint, deductibles are there for a reason. They help:

- Share risk between the insurer and the policyholder

- Reduce very small claims

- Help control premiums overall

- Give drivers some flexibility in how they structure their policy

This is why deductible choice matters. It directly affects both price and claim behaviour.

How Do Car Insurance Deductibles Work?

The easiest way to understand a deductible is to think of it as your share of a covered claim.

It commonly comes into play when:

- You are at fault in an accident

- Your vehicle is damaged in a collision

- Your vehicle is stolen

- Your car is vandalized

- Weather or hail damage

It usually does not apply in the same way when:

- You are not at fault and the claim is handled accordingly

- The claim is for liability coverage

- Another part of the policy responds without a deductible applying

Ontario’s auto insurance system can make this confusing because drivers deal with their own insurer first, but fault still matters when determining how deductibles apply.

When Do You Pay a Car Insurance Deductible?

You generally pay your deductible when you make a claim that includes one. That usually means:

- The claim is approved

- Repairs are being completed

- The amount is paid to the repair shop or deducted from your settlement

If the cost of damage is below or only slightly above your deductible, filing a claim may not make much financial sense.

For example if your deductible is $1,000 and the repair cost is $1,150, you would only receive limited value from the claim, and the claim itself could still affect your record or future pricing.

That is one reason drivers should not think about deductibles in isolation. The deductible amount affects whether it is worth using your insurance at all for smaller losses.

Get a quote to review your deductible, premium, and how your policy would respond in a real claim.

What Types of Car Insurance Deductibles Are There?

In Ontario auto insurance, the most common deductible categories are tied to the type of physical damage coverage you have.

Collision deductible

This usually applies when your vehicle is damaged in an accident involving:

- another vehicle

- a guardrail

- a pole

- another object

- a rollover

Comprehensive deductible

This usually applies to non-collision losses such as:

- theft

- attempted theft

- vandalism

- fire

- hail

- falling objects

- some weather-related damage

All perils coverage

This combines features of collision and comprehensive coverage and is often used for newer or financed vehicles.

Different coverages can carry different deductibles, which is why two policies that look similar at first glance may behave differently when you actually file a claim.

High Deductible vs Low Deductible Car Insurance

This is really a tradeoff between lower premiums now and higher out-of-pocket costs later.

A high deductible usually means:

- lower premium

- more financial responsibility if you file a claim

- fewer small claims are worth submitting

A low deductible usually means:

- higher premium

- less out-of-pocket cost after a claim

- easier short-term claim affordability

Neither is automatically better. The right choice depends on your budget, driving habits, vehicle value, and tolerance for financial risk.

Is a $1,000 Deductible Good for Car Insurance?

For many Ontario drivers, yes, a $1,000 deductible can be a reasonable middle ground. It may make sense if:

- you want to reduce your premium

- you have emergency savings

- you have a clean driving record

- you do not expect to make small claims

It may be less suitable if:

- paying $1,000 unexpectedly would create financial stress

- you prefer more predictable costs after a loss

- you drive in higher-risk conditions and want lower out-of-pocket exposure

In Ontario, this question comes up often because many drivers have newer vehicles, higher repair costs, and commuting patterns that make coverage decisions more important.

How Much Is My Car Insurance Deductible?

Your deductible is shown in your policy documents, usually under the sections for:

- collision coverage

- comprehensive coverage

- optional endorsements if applicable

If you are not sure what your deductible is, the most direct ways to check are:

- review your policy declaration page

- review your renewal paperwork

- ask your broker to walk through the coverage with you

A lot of drivers know their premium but do not actually know their deductible. That becomes a problem only once a claim happens.

Why Deductibles Matter More Than Drivers Think

Many people think of the deductible as just a pricing lever. It is that, but it also affects broader insurance strategy.

Deductibles influence:

- how much you pay annually

- whether a claim is worth filing

- how much you pay out of pocket after a loss

- how comfortable you feel carrying the policy you chose

This is why a cheaper premium is not always the better result. If the deductible is too high for your finances, the savings may not feel worthwhile when something goes wrong.

Car Insurance Deductible Trends in Ontario

While deductibles vary by insurer and vehicle, many Ontario drivers land in a fairly common range.

Typical patterns include:

- $500 as a common baseline deductible

- $1,000 as a frequent middle-ground choice

- $2,000 or higher for drivers prioritizing premium reduction

Here is a simple comparison:

The real takeaway is not just that higher deductibles lower premiums. It is that the right deductible depends on whether the savings actually justify the added risk.

Local Perspective: Oakville and Halton Region

Deductible decisions are also influenced by local driving conditions and vehicle ownership patterns.

For drivers in Oakville and Halton Region, a few things often matter:

- many households insure relatively newer vehicles

- repair costs can be higher than expected

- some drivers commute into busier surrounding areas

- others use their vehicles more locally and less intensively

That means deductible choice is often a balancing act between:

- keeping premiums reasonable

- protecting against higher repair bills

- making sure a claim would still be manageable financially

This is one reason why a deductible review is worth doing periodically. What made sense a few years ago may not make sense now.

Get a quote to compare deductible options with guidance tailored to your vehicle and driving profile.

Why Many Policies Fall Short

Most businesses and homeowners have coverage, but it does not always reflect real-world exposure. Common issues include:

- Coverage based on outdated property values

- Deductibles that are too high relative to risk

- Missing endorsements or incomplete auto coverage

- No consideration for operational downtime

These gaps are usually only discovered during a claim.

How Car Insurance Deductibles Affect Premiums and Claim Costs

In Ontario, choosing a lower deductible usually means paying a higher premium, while choosing a higher deductible usually lowers your premium but increases what you pay yourself if you make a claim. The best option often depends on whether you want lower monthly costs or more protection when an accident happens.

| Deductible | What Changes | Who It Suits |

|---|---|---|

| $500 | Usually comes with a higher premium, but it keeps your out-of-pocket cost lower if you need to make a claim. This option offers more financial protection at claim time. | Drivers who want more predictable costs and prefer not to pay a large amount upfront after an accident. |

| $1,000 | Often creates a middle-ground balance between premium savings and claim-time cost. You pay less in premium than with a lower deductible, but still avoid the highest out-of-pocket exposure. | Drivers looking for a practical balance between affordability and manageable financial risk. |

| $2,000+ | Usually lowers your premium more noticeably, but increases your financial responsibility if you make a claim. This can save money over time, but only if the higher deductible is affordable when needed. | Drivers with strong emergency savings who are comfortable taking on more risk in exchange for lower premiums. |

This comparison is general and may vary by insurer, vehicle, driving history, and location in Ontario, including Oakville and Halton Region.

How to Choose the Right Deductible

Choosing the right deductible is about balancing your premium with what you could afford to pay if you make a claim.

- Make sure it’s affordable: Choose an amount you could comfortably pay out of pocket if needed.

- Consider how you’d use your insurance: If you’d only claim for major damage, a higher deductible may make sense.

- Think about your vehicle’s value: Older vehicles may not justify higher premiums for a low deductible.

- Factor in your driving habits: More time on the road or commuting may justify a lower deductible.

- Don’t focus only on price: A lower premium isn’t always better if the deductible is too high to manage.

The goal is to find a deductible that fits both your budget and your real-world risk.

What Drivers Often Miss About Deductibles

There are a few points that drivers regularly overlook:

- different coverages can have different deductibles

- a claim that is only slightly above the deductible may not be worth filing

- lower premiums often come with more retained risk

- policy reviews should include deductibles, not just total premium

- deductible choice should match current finances, not old assumptions

These details matter because they influence claim decisions and overall policy value.

Visual: Navigating Car Insurance Deductibles (The Ontario Driver’s Guide)

Why Work With James Inwood

James Inwood works with drivers across Oakville, Halton Region, and Ontario who want clearer advice on how their auto insurance actually works.

Deductibles are a good example of where quick online comparisons can fall short. It is easy to focus on price, but the more important question is how the policy responds when something happens.

James’ approach focuses on:

- reviewing deductible options in context

- comparing policies beyond price alone

- identifying where coverage structure changes the real value

- helping drivers choose protection that fits their budget and real-world risk

For drivers who want more than a surface-level quote, that kind of guidance can make a meaningful difference.

Get a quote or book a quick call to review your deductible and compare car insurance with more clarity.

Frequently Asked Questions

No. A deductible only applies to certain types of claims, typically collision or comprehensive. If you are not at fault and the claim is handled accordingly, your deductible may be waived depending on the situation and insurer.

Yes. Your deductible can be adjusted when you renew your policy or update your coverage. Some insurers also offer options like disappearing deductibles that decrease over time if you remain claim-free.

Increasing your deductible can reduce your premium, but it only makes sense if you are comfortable covering that amount yourself. The savings should be weighed against the financial impact of a potential claim.

If the repair cost is below your deductible, you would typically pay the full amount out of pocket and not involve your insurer. In many cases, filing a claim for a small difference is not worth it.

James Inwood is an Oakville-based insurance broker who helps drivers across Halton Region and Ontario understand how car insurance works in practical terms. His work focuses on real coverage decisions, including deductibles, policy structure, and claim outcomes.

His approach is advisory and straightforward, helping clients understand the difference between a lower price and a better policy.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn