How to Lower Car Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

How to Lower Car Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Car insurance is one of the most common recurring expenses for drivers across Ontario. While premiums vary based on several factors, many drivers are surprised by how much their own decisions can influence the final cost.

For drivers in Oakville and across Halton Region, factors such as commuting patterns, vehicle choice, driving history, and even where a vehicle is parked overnight can affect how insurers calculate risk.

Understanding how these factors work can help drivers make informed decisions and potentially reduce their insurance premiums while maintaining strong coverage.

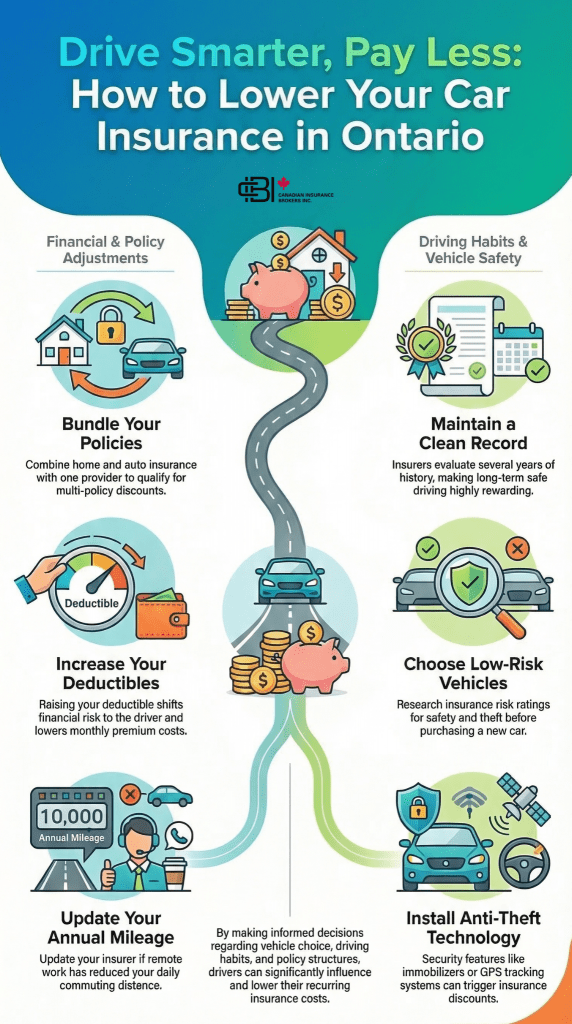

At a Glance: How to Save On Car Insurance

Lowering car insurance premiums in Ontario usually comes down to a handful of practical decisions. Drivers often see meaningful savings when they:

- Compare insurance quotes before renewal

- Bundle home and auto insurance policies

- Increase deductibles where appropriate

- Maintain a clean driving record

- Drive fewer kilometres annually

- Choose vehicles with lower insurance risk ratings

- Install anti theft or vehicle tracking devices

Quick Reference Guide to Lowering Car Insurance

Drivers can often lower their insurance premiums by focusing on a few key factors that insurers consider when pricing policies.

- Maintain a clean driving record: Fewer accidents and violations reduce claim risk and help keep premiums lower.

- Choose a higher deductible: Increasing the deductible shifts more risk to the driver and can lower premiums.

- Bundle insurance policies: Combining home and auto insurance may qualify drivers for multi-policy discounts.

- Drive fewer kilometres each year: Less time on the road reduces accident exposure.

- Choose vehicles with lower insurance risk: Cars with strong safety ratings and lower theft rates tend to cost less to insure.

- Install anti theft devices: Security features such as immobilizers or tracking systems can reduce theft risk.

Insurance savings usually come from a combination of these adjustments rather than a single change. If you want to see how your current policy compares with other available options, you can get a quote and review policies that match your situation.

Why Lowering Car Insurance Usually Comes Down to Risk

Many drivers assume insurance premiums are mostly determined by discounts. In practice, insurers primarily price policies based on risk. Discounts exist, but they usually have a smaller effect than the underlying factors insurers use to evaluate drivers.

In conversations with drivers in Oakville, one of the most common misconceptions is that switching companies alone will dramatically reduce premiums. While comparing quotes can help, insurers ultimately base pricing on the likelihood of a future claim.

Factors such as driving behaviour, vehicle choice, mileage, and claims history all influence how insurers calculate that risk. Once drivers understand this, the strategies for lowering insurance become clearer.

Some strategies focus on prevention, but others protect your rate after a claim. Accident forgiveness is one option that helps limit premium increases after your first at-fault accident.

Why Many Ontario Drivers Overpay

One issue that appears frequently when reviewing policies is outdated information.

For example, a driver who once commuted daily into Toronto may now work remotely several days per week. If annual mileage estimates have not been updated, the insurer may still be pricing the policy based on higher driving exposure.

The same applies to other details. Parking arrangements, additional drivers in a household, and vehicle usage sometimes change without being reflected in the policy. New drivers often face higher premiums, so it’s helpful to review car insurance for G2 drivers in Ontario to understand how experience level impacts pricing and available discounts.

These details may seem small, but they influence how insurers evaluate risk. Reviewing policy details periodically ensures premiums reflect current circumstances rather than outdated assumptions.

The Long Term Value of a Clean Driving Record

Driving history remains one of the most important factors affecting insurance premiums.

A clean driving record signals lower claim probability. Drivers who go several years without accidents or traffic violations often begin to see noticeable reductions in premiums.

One point many drivers overlook is how long insurers evaluate driving history. Insurance companies often consider several years of records rather than only the most recent renewal period. Avoiding even minor violations can have long term benefits when it comes to insurance pricing.

Choosing Vehicles That Are Cheaper to Insure

Vehicle choice can influence insurance premiums more than many drivers expect.

Insurers evaluate vehicles using several factors including:

- theft frequency

- repair costs

- safety ratings

- historical claims data

Vehicles that are expensive to repair or frequently targeted by theft often carry higher insurance risk ratings.

For drivers in Oakville considering a new vehicle, checking insurance implications before purchasing can prevent unexpected costs later. Even a small difference in insurance risk rating can affect premiums for years.

Adjusting Deductibles to Reduce Premiums

Insurance deductibles represent the amount a driver pays before insurance coverage applies after a claim. Increasing a deductible can lower premiums because it shifts part of the financial risk back to the driver.

Many drivers underestimate how flexible deductibles can be. As financial circumstances change, adjusting deductible levels may become a practical way to reduce insurance costs For drivers who have maintained claim free records for several years, reviewing deductible options can be worthwhile.

Bundling Home and Auto Insurance

Bundling multiple insurance policies with the same insurer is one of the most common ways to lower premiums.

Drivers who combine policies such as:

often qualify for multi policy discounts.

For homeowners across Oakville and Halton Region, bundling policies can simplify insurance management while reducing overall costs.

Driving Less Can Lower Insurance

Insurance companies pay close attention to how frequently vehicles are on the road. Drivers who travel fewer kilometres statistically face lower accident risk.

Commuting patterns in Oakville often influence annual driving distance. Some residents commute into Toronto or Mississauga, while others work locally or remotely.

Drivers who have shifted to hybrid or remote work sometimes find they drive far fewer kilometres than before. Updating mileage estimates with insurers can occasionally reduce premiums.

Anti Theft Measures That Can Reduce Insurance Costs

Vehicle theft has become an increasingly important factor in insurance pricing. Cars equipped with anti theft technology are often considered lower risk.

Common security measures include:

- immobilizers

- GPS tracking systems

- steering wheel locks

These devices can help protect vehicles and may also qualify drivers for insurance discounts. Drivers who park vehicles in garages or secured areas may also benefit from reduced theft risk.

Usage Based Insurance Programs

Technology is gradually changing how insurers evaluate driving behaviour. Usage based insurance programs track driving patterns through mobile apps or small devices installed in vehicles.

These programs often monitor:

- braking patterns

- acceleration habits

- nighttime driving

- total kilometres driven

Drivers who demonstrate safe driving behaviour may qualify for insurance discounts.For drivers who travel shorter distances or drive cautiously, these programs can provide measurable savings.

Practical Ways to Save On Car Insurance

There are several practical ways Ontario drivers can reduce their car insurance premiums. While savings vary by insurer and driver profile, the strategies below are among the most common ways to help lower costs.

| Way to Lower Insurance | Common Ontario Example | Why It Can Help |

|---|---|---|

| Maintain a clean driving record | Avoiding accidents, tickets, and at-fault claims | Insurers reward lower-risk drivers with better rates |

| Choose a lower-risk vehicle | Driving a model with lower theft rates and lower repair costs | Cars that are cheaper to repair or less likely to be stolen often cost less to insure |

| Reduce annual kilometres | Driving less by working from home or using transit part-time | Less time on the road can mean lower accident exposure |

| Bundle insurance policies | Combining home and auto coverage with the same insurer | Many insurers offer multi-policy discounts |

| Increase your deductible | Choosing a higher deductible to reduce monthly premium costs | A higher deductible usually lowers the insurer’s risk on smaller claims |

| Ask about discounts | Using winter tires, telematics, alumni, or employer group discounts | Available discounts can reduce premiums without changing coverage needs |

Learn more about what influences car insurance prices in Ontario.

How Driving Behaviour Data Is Influencing Insurance Pricing

A 2024 study from Toronto Metropolitan University’s Ted Rogers School of Management examined how telematics data can improve how insurers assess driver risk. The research analyzed driving behaviour data such as braking patterns, acceleration, and kilometres driven.

The study found that incorporating real driving behaviour helps insurers better predict claim risk and price policies more accurately.

This matters because several insurers in Canada now offer usage based insurance programs, where safe driving habits may lead to lower premiums over time.

Common Mistakes That Increase Car Insurance

Many drivers focus on finding discounts but overlook small details that can quietly increase premiums. Common issues include:

- Not updating annual mileage: Changes in commuting habits may not be reflected in the policy.

- Choosing vehicles with high theft rates: Some vehicles are stolen more frequently and carry higher insurance risk.

- Allowing policies to renew automatically: Drivers may miss chances to review coverage or compare options.

- Keeping outdated coverage levels: Older vehicles may not need the same coverage as newer ones.

Avoiding these mistakes can sometimes reduce insurance costs without major changes to coverage. If your policy hasn’t been reviewed recently, it may be worth taking a moment to get a quote and see what options are available today.

Lowering Insurance After an Accident

An accident does not permanently define a driver’s insurance profile. While premiums often increase following a claim, the impact usually decreases over time as new driving history replaces older incidents.

Drivers who maintain safe driving habits and avoid further violations gradually rebuild favourable risk profiles. Consistent safe driving often helps restore more competitive insurance pricing.

Visual: How to Lower Your Car Insurance in Ontario

Finding the Best Car Insurance Broker in Ontario

Car insurance needs can change over time as drivers move, buy new vehicles, adjust commuting habits, or update their coverage. Reviewing your policy periodically can help ensure it still reflects how your vehicle is actually used.

Working with an independent broker like James Inwood can make this process easier. Based in Oakville, James has been helping Ontario clients since 2010 and works with multiple insurance providers, making it easier to compare coverage options and pricing from different insurers.

For drivers in Oakville and across Halton Region, this can provide a clearer view of available policies and help identify coverage that better fits their current needs.

If you’d like to review your options, you can get a quote to explore available insurance solutions.

Frequently Asked Questions

Insurance rates may decrease after several years of claim-free driving, but the change is not always automatic. Insurers periodically reassess driver risk based on claims history, driving record, and policy details. Reviewing coverage at renewal helps ensure premiums reflect current circumstances.

Working from home often reduces annual driving distance. Because insurers consider kilometres driven when evaluating risk, updating mileage estimates can sometimes lower premiums if the vehicle is being used less frequently than before.

Newer vehicles do not always cost more to insure. While repair costs can be higher for some models, modern safety features such as collision avoidance systems and advanced braking technology may reduce accident risk and influence insurance pricing.

Parking location influences how insurers evaluate risk. Vehicles parked in garages or secured parking areas typically face lower theft and damage risk compared with vehicles parked on the street overnight.

Insurance policies are usually best reviewed once a year. Changes such as moving, purchasing a new vehicle, changing commuting habits, or adding drivers to a household can all influence how a policy should be structured.

James Inwood is a Canadian insurance advisor and editor specializing in personal and commercial insurance across Ontario. Based in Oakville, his work focuses on helping individuals and businesses understand how insurance policies respond in real world situations and how drivers can make practical decisions that reduce risk and insurance costs.

He advises clients throughout Oakville and Halton Region, with particular attention to everyday insurance questions that often arise during renewals, claims, and policy reviews.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn