Luxury Car Insurance in Oakville

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Luxury Car Insurance in Oakville

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Luxury vehicles are insured differently than standard vehicles because the financial exposure is different from the start. Repair costs, imported parts, theft trends, performance capability, and vehicle value all affect how insurers evaluate risk.

In Oakville, luxury vehicle ownership can include daily-use luxury SUVs, seasonal sports cars, imported performance vehicles, electric luxury cars, and collector vehicles. Each one can require a different insurance structure.

The goal is not just to insure a more expensive vehicle. It is to make sure the policy reflects how the vehicle is used, stored, valued, and repaired if a claim happens.

At a Glance: Luxury Car Insurance

- Designed for high value, exotic, collector, and performance vehicles

- Repair costs and theft exposure can strongly affect pricing

- Agreed value coverage may be available for rare or collector vehicles

- Luxury SUVs and electric luxury cars may need broader coverage review

- Imported vehicles may require specialty underwriting

- Multi vehicle policies may help households with several premium vehicles

- Coverage should reflect vehicle value, usage, storage, and repair needs

What Is Luxury Car Insurance?

Luxury car insurance is coverage designed for vehicles that carry higher financial risk than a typical passenger vehicle. The policy still follows auto insurance requirements, including liability coverage, accident benefits, and optional physical damage coverage. The difference is how insurers assess the vehicle itself.

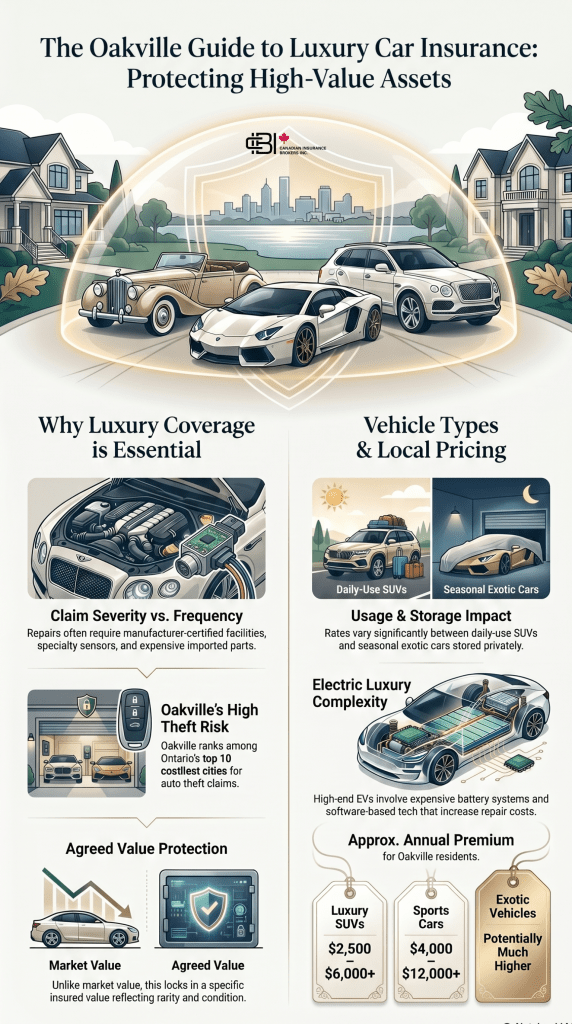

A small claim on a luxury vehicle can become expensive because repairs may involve specialty parts, sensors, cameras, advanced safety systems, custom paint, or manufacturer-certified repair facilities.

Because of this, insurers may look closely at vehicle value, theft exposure, annual mileage, garage storage, driver history, and whether the vehicle is used daily or seasonally.

Why Luxury Vehicles Cost More to Insure

Luxury car insurance does not cost more simply because the vehicle is expensive. The premium usually reflects the cost and complexity of repairing or replacing the vehicle after a claim.

For example, a damaged bumper on a luxury SUV may involve more than bodywork. It may also require camera replacement, sensor calibration, specialty parts, and labour from a certified repair facility.

This is why high end vehicle insurance often focuses on claim severity. The risk is not only whether a claim happens, but how expensive the claim could become.

Biggest Factors Affecting Luxury Car Insurance

Theft Exposure

Luxury SUVs and imported vehicles may face higher theft exposure across Ontario.

Repair Costs

Advanced sensors, imported parts, and specialized labour can increase claim severity.

Vehicle Performance

Higher horsepower and performance capability can affect underwriting.

Replacement Value

Limited production and specialty vehicles may carry higher replacement costs.

Pricing varies based on underwriting, claims history, storage conditions, and vehicle usage.

How Much Does Luxury Car Insurance Cost in Oakville?

Luxury vehicle insurance costs vary depending on the vehicle, driver profile, claims history, storage, and usage.

Approximate annual ranges in Oakville may include:

- Luxury SUVs: approximately $2,500 to $6,000+

- Sports cars: approximately $4,000 to $12,000+

- Exotic vehicles: potentially much higher

- Collector vehicles: varies based on agreed value, storage, and usage

The best way to estimate pricing is through a luxury car insurance quote based on the exact vehicle, driver, location, and coverage structure.

Get a quote to compare luxury vehicle insurance options based on your vehicle and driving habits.

Agreed Value vs Replacement Value Luxury Car Insurance

One of the most important parts of luxury car insurance is how the vehicle is valued after a major claim.

With a standard policy, a total loss is often settled based on market value at the time of the loss. For some luxury vehicles, that may not fully reflect rarity, condition, modifications, restoration quality, or collector demand.

Agreed value coverage allows the insurer and vehicle owner to agree on a specific insured value before a loss occurs. This is often used for collector cars, classic luxury vehicles, rare imports, restored vehicles, and some exotic cars.

Replacement value coverage is different. It may apply to newer eligible vehicles and can help replace the vehicle with a new comparable model after a covered total loss, depending on policy wording.

Get a quote to compare agreed value and replacement value options for your luxury vehicle.

Luxury SUV Insurance

Luxury SUVs are one of the most common high value vehicle categories in Ontario. Models such as Range Rover, Mercedes-Benz GLS, BMW X7, Porsche Cayenne, Lexus LX, and Cadillac Escalade can carry higher insurance costs because of replacement value, theft exposure, and expensive technology.

Many luxury SUVs are also daily-use vehicles. That means insurers may consider commuting patterns, annual mileage, parking location, and whether the vehicle is stored in a garage overnight.

For Oakville households with larger driveways or multiple vehicles, it may also be worth reviewing how each vehicle is insured within the overall household policy structure.

Sports Car and Exotic Car Insurance

Sports car insurance and exotic car insurance often involve more specialized underwriting than standard auto insurance.

These vehicles may have higher horsepower, limited production parts, lower ground clearance, specialized repair requirements, and higher replacement values. A Lamborghini, Ferrari, McLaren, Aston Martin, or Porsche 911 may need coverage that reflects both performance exposure and repair complexity.

Some exotic vehicles are driven only seasonally, while others are used more often. This difference matters. Limited-use vehicles may qualify for different insurance structures than vehicles driven regularly.

Collector and Classic Luxury Car Insurance

Collector car insurance works differently than daily driver insurance because the vehicle is usually not used the same way.

A classic luxury car may be stored indoors, driven only during warm months, and maintained as an investment or hobby vehicle. Insurers may request an appraisal, photos, storage details, and estimated annual mileage.

Collector coverage may offer agreed value structures, but it can also include restrictions on commuting, business use, winter driving, or mileage. The goal is to match the coverage to how the vehicle is actually owned and used.

Electric Luxury Car Insurance

Electric luxury vehicles add another layer of complexity. High value electric vehicles may include expensive battery systems, advanced sensors, software-based technology, and specialized repair requirements.

Vehicles such as higher-end Tesla models, Porsche Taycan, Lucid, Mercedes EQ, and BMW electric models may cost more to repair after a claim than many gas-powered vehicles in the same price range.

Charging equipment, home garage setup, battery exposure, and parts availability can all affect how the vehicle is reviewed by insurers.

Coverage for Imported Luxury Cars

Imported luxury cars can often be insured in Ontario, but the process may require more review.

Insurers may look at whether the vehicle meets Canadian import requirements, whether replacement parts are available, whether local repair facilities can service the vehicle, and how the vehicle should be valued.

This matters for rare imports, right-hand-drive vehicles, limited production models, and specialty performance vehicles. In some cases, an appraisal or specialty insurer may be needed before coverage is approved.

Luxury Vehicle Insurance Comparison

Case Study: Luxury Vehicle Theft in Ontario

Luxury vehicle theft remains a major insurance concern in Ontario. The Insurance Bureau of Canada reported that Ontario’s auto theft claims costs were $485 million in 2025, and Oakville ranked among the province’s top 10 costliest cities for auto theft claims.

A recent Ontario investigation called Project Starter recovered 40 stolen vehicles worth more than $3 million, including luxury models such as a Lamborghini and multiple Lexus RX vehicles.

For luxury vehicle owners, this shows why comprehensive coverage, replacement value options, anti-theft protection, and proper policy structure matter.

Get a quote to review comprehensive coverage and theft protection options for your luxury vehicle.

Multi Vehicle Luxury Car Insurance

Some households insure more than one high value vehicle. This may include a luxury SUV, an electric luxury car, a sports car, and a seasonal collector vehicle.

A coordinated multi vehicle policy structure can make coverage easier to manage. It may also help align deductibles, drivers, usage, storage, and optional coverage across the household.

This does not mean every vehicle should be insured the same way. A daily-use luxury SUV may need a different structure than a classic vehicle stored for most of the year.

Why Work With James Inwood

Luxury vehicle insurance involves more than simply insuring a higher-priced vehicle. Repair exposure, theft trends, agreed value structures, imported parts, storage, and vehicle usage all affect how coverage performs during a claim.

James Inwood works with drivers across Oakville and throughout Ontario reviewing insurance options for luxury SUVs, sports cars, collector vehicles, imported vehicles, and high value auto collections.

Get a quote or book a meeting with James Inwood to compare luxury car insurance options based on your vehicle type, value, and usage.

Frequently Asked Questions

Luxury car insurance often costs more because the vehicle is more expensive to repair, replace, and protect against theft. Insurers may also consider advanced safety systems, imported parts, specialty labour, and claim severity. A damaged sensor, camera, windshield, or body panel on a luxury vehicle can cost significantly more than the same repair on a standard car.

Agreed value coverage may be available for collector cars, rare imports, restored vehicles, classic luxury cars, and some exotic vehicles. The insurer and owner agree on the insured value before a loss occurs, often using appraisals, photos, purchase records, or documentation of restoration work. This can provide more certainty during a total loss claim.

Imported luxury vehicles can require more underwriting review because parts availability, repair access, vehicle valuation, and Canadian compliance can be more complex. Insurers may ask for import documents, appraisals, inspection details, or proof that the vehicle can be serviced properly in Ontario. Some vehicles may need specialty insurance markets.

Modifications can affect both insurance pricing and claim settlement. Performance upgrades, custom wheels, wraps, body kits, suspension changes, exhaust work, or premium audio systems should be disclosed to the insurer. If upgrades are not listed properly, they may not be fully covered after a claim.

James Inwood is an Ontario-based insurance broker who works with drivers across Oakville reviewing insurance options for luxury vehicles, sports cars, collector vehicles, imported vehicles, and high value automotive collections. He helps clients understand how insurance applies to real ownership situations, including agreed value coverage, replacement exposure, specialty repairs, imported parts, theft risk, and luxury vehicle underwriting.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn