Understanding Business Interruption Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Understanding Business Interruption Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Business interruption insurance protects a business when it cannot operate due to a covered loss. While physical damage is often the focus, the financial impact that follows is usually more significant.

Across Ontario, a disruption can last months. During that time, revenue stops while expenses continue, creating pressure on cash flow and recovery.

This is where business interruption insurance becomes essential. It helps stabilize the business and supports operations while repairs are completed.

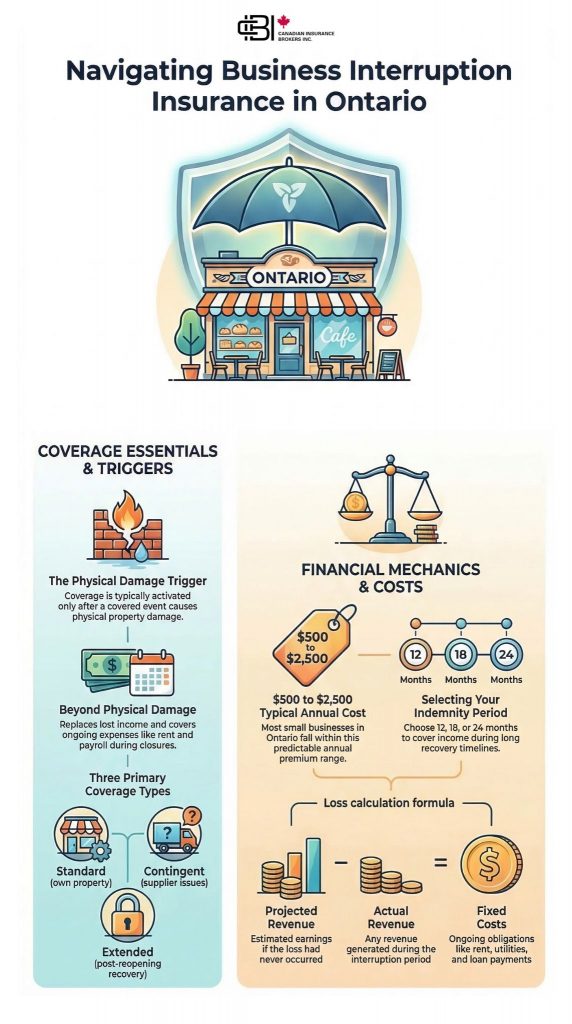

At a Glance: Business Interruption Insurance in Ontario

Business interruption insurance is designed to protect income, but how it works depends on how the policy is structured.

- Replaces lost income when your business cannot operate

- Covers ongoing expenses like rent and payroll

- Typically included within commercial property insurance

- Usually requires physical damage to trigger coverage

- Based on projected income, not just current revenue

- Indemnity period determines how long coverage applies

Business Interruption Insurance Meaning & Definition

Business interruption insurance is coverage that replaces lost income and helps pay ongoing expenses when a business is forced to pause operations due to a covered event.

In Ontario, this coverage is usually included as part of a commercial property policy rather than purchased on its own.

Unlike property insurance, which focuses on repairing physical damage, this coverage focuses on the financial impact of downtime. It is designed to put the business in the position it would have been in if the loss had not occurred.

It is typically used by lenders to confirm a home is worth the amount being financed. The appraiser considers factors like location, condition, size, and recent sales of similar properties.

An appraisal measures market value, not rebuild cost. This is why homeowners often review their insurance coverage at the same time, since insurance is based on what it would cost to rebuild the home, not what it could sell for.

How Business Interruption Insurance Works in Ontario

Business interruption insurance is triggered when a covered event causes physical damage that interrupts operations.

In practical terms, this means a business must first experience damage that is covered under its property policy. Once that happens, the interruption coverage responds to the financial loss that follows.

For example, a fire in a commercial space in Oakville may take several months to repair. During that time, the business may be unable to operate. Revenue stops, but expenses continue.

This structure is common across Ontario. A restaurant in Toronto, a contractor in Halton Region, or a retail store in Mississauga may all rely on this coverage if operations are interrupted.

When a home is purchased, refinanced, or updated, this is typically when homeowners revisit their coverage. Changes in materials, renovations, or construction costs can affect how much protection is needed, even if the market value changes for different reasons.

For many homeowners in Ontario, this is the point where they compare what their home is worth on the market with what it would take to rebuild it, helping ensure coverage remains aligned with the property itself.

What Does Business Interruption Insurance Cover?

In most cases, business interruption coverage includes:

- Lost income based on expected earnings

- Ongoing expenses such as rent, utilities, and loan payments

- Payroll for key employees

- Additional costs to reduce downtime, such as temporary space or equipment

The exact scope depends on how the policy is structured, but the goal remains the same. Keep the business financially stable while it recovers.

Get a quote to compare coverage options based on your operations and risk level.

Types of Business Interruption Insurance

There are several variations of business interruption coverage, and the differences can affect how a claim responds.

- Standard business interruption: applies when your own property is damaged

- Contingent business interruption: applies when a supplier or partner is affected

- Extended business income: continues after reopening while revenue returns to normal

These distinctions are not always obvious at the time of purchase, but they can make a significant difference during a claim.

How Business Interruption Insurance Is Calculated

Business interruption claims are based on financial data rather than simple estimates.

At a basic level, insurers look at:

- The difference between projected and actual revenue

- Ongoing expenses that continue during the interruption

- Financial trends, seasonality, and growth

Loss = (Projected Revenue – Actual Revenue) + Fixed Costs

This is why accurate financial records are important. The more clearly a business can demonstrate expected income, the more precise the claim calculation will be.

The Indemnity Period in Business Interruption Insurance

The indemnity period defines how long the policy will cover lost income after a claim.

Common options include:

- 12 months

- 18 months

- 24 months

In Ontario, recovery timelines can extend due to permitting, construction delays, or supply chain issues. If the indemnity period is too short, coverage may end before the business is fully operational again.

Business Interruption Insurance Claims

The claims process involves both property damage and financial review. After a loss, the insurer evaluates the damage and the financial impact. This includes reviewing past performance, expenses, and projections.

Businesses are typically required to provide:

- Financial statements

- Tax returns

- Payroll records

- Expense breakdowns

What Is Not Covered by Business Interruption Insurance

Business interruption insurance does not apply to every type of disruption.

Most policies require physical damage to trigger coverage. Common exclusions include:

- Pandemics or widespread shutdowns

- Utility outages outside the property

- Cyber incidents

- Undocumented income

Understanding these limitations is important when reviewing or structuring coverage.

Business Interruption Insurance Cost in Ontario

The cost of coverage depends on the size and type of business, as well as how the policy is structured.

For many small businesses in Ontario, business interruption coverage is included within a broader commercial policy and falls within a predictable range.

Typical range:

- Small businesses: $500 to $2,500 annually

- Larger businesses: $5,000+ depending on risk and size

What matters most is not just the premium, but whether the coverage reflects the actual financial impact of an interruption.

Get a quote and review options based on your industry, revenue, and coverage needs.

Because appraisals are often tied to mortgage approvals or refinancing, this is also when many homeowners revisit their insurance coverage to ensure everything is aligned before moving forward.

How Business Interruption Insurance Protects Ontario Businesses

| Business Situation | What Happens Without Coverage | What Business Interruption Insurance Helps Cover | Why It Matters |

|---|---|---|---|

| Fire forces temporary closure | Revenue stops while fixed expenses continue | Lost income, rent, payroll, and ongoing operating costs | Helps the business stay financially stable during repairs |

| Water damage interrupts operations | Unexpected downtime and delayed reopening | Income loss during closure and certain extra recovery expenses | Reduces the financial pressure caused by a prolonged shutdown |

| Temporary relocation is required | Additional out-of-pocket costs to continue serving clients | Costs related to operating from a temporary location | Supports continuity while the original premises are restored |

| Repairs take longer than expected | Coverage can run out if the indemnity period is too short | Income replacement during the covered recovery period | Shows why policy structure matters as much as having coverage |

Why Many Businesses Are Underinsured

Many businesses do have business interruption coverage, but it does not always reflect their real exposure.

This often comes down to how the policy was set up. Revenue may be underestimated, growth may not be considered, and recovery timelines may be shorter than what actually occurs. Common issues include:

- Coverage based on past revenue without factoring in growth

- Indemnity periods that are too short

- Policies not updated as the business evolves

Months later, a water damage claim affected part of the renovated area. Because the policy limits were based on the older structure and lower rebuild estimate, not all of the repair costs were fully covered.

Situations like this show how appraisal changes can highlight gaps between a home’s current condition and its insurance coverage. When a property’s value shifts, it is often a good time to review whether the policy still reflects how the home is actually built and used today.

Why Business Interruption Insurance Matters

Business interruption insurance becomes most important in the period after a loss, when uncertainty around timelines and costs starts to build.

Even with repairs underway, businesses are often dealing with delays, shifting schedules, and pressure to maintain relationships with clients and employees. Without a financial buffer, these challenges can compound quickly.

This coverage provides stability during that period, allowing business owners to focus on getting operations back on track rather than managing short-term financial strain.

Visual: Navigating Business Insurance in Ontario

Why Work With James Inwood?

James Inwood is an insurance broker based in Oakville who works with business owners across Halton Region and Ontario.

He focuses on how businesses actually operate and how risk shows up in real situations. Rather than using generic policies, he aligns coverage with how the business runs and how exposure develops over time.

Get a quote or book a quick call to review your current coverage and identify any gaps.

Frequently Asked Questions

Business interruption coverage typically begins after a covered loss causes a disruption to operations. Some policies include a short waiting period, often 24 to 72 hours, before payments start.

Property insurance covers physical damage to your building or equipment. It does not replace lost income. Business interruption insurance is what helps cover the financial impact while your business is unable to operate.

The duration of a claim depends on the indemnity period selected in your policy and how long it takes your business to recover. In many cases, payments continue until operations return to normal or the policy limit is reached.

Yes, and in many cases, smaller businesses are more vulnerable to interruptions because they rely on consistent cash flow. Even a short shutdown can have a significant financial impact without coverage.

The right amount of coverage depends on several factors, including your revenue, fixed expenses, and how long it would realistically take to recover from a disruption. Growth and seasonality should also be considered when setting limits.

It is not legally required, but it is commonly included as part of a commercial insurance policy. Many business owners choose to include it because of the financial risks associated with downtime.

James Inwood is a Canadian insurance advisor specializing in commercial insurance for contractors, trades, and small business owners across Ontario. Based in Oakville, he works closely with clients to help them understand how risk, liability, and insurance connect in real business situations.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn