Cargo Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Cargo Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Cargo insurance helps Ontario businesses protect goods from damage, theft, delay, or loss while in transit. It is important for freight brokers, trucking companies, manufacturers, importers, exporters, distributors, and logistics providers moving goods between warehouses, ports, rail terminals, distribution centres, and customers.

As supply chains become more complex across Oakville, the GTA, Canada, and international markets, cargo insurance plays a key role in managing transportation risk.

At a Glance: Cargo Insurance

- Helps protect goods while in transit

- Used by trucking companies, freight brokers, importers, exporters, and distributors

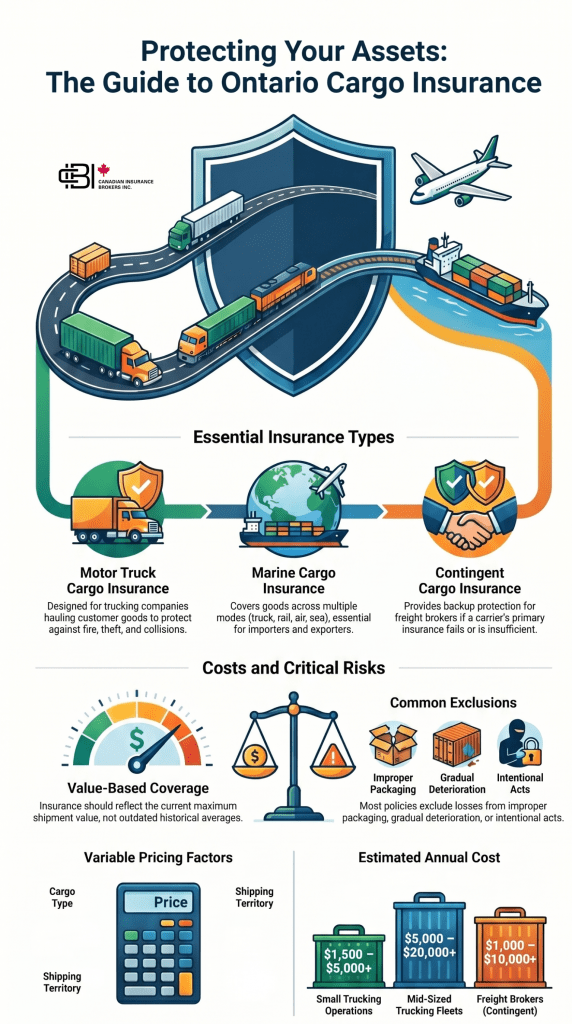

- Motor truck cargo insurance is common for trucking operations

- Marine cargo insurance can apply to international and domestic shipments

- Contingent cargo insurance is often used by freight brokers

- Costs vary based on cargo value and transportation exposure

- Coverage should reflect how goods move through the supply chain

What Is Cargo Insurance?

Cargo insurance is designed to protect goods while they are being transported. If cargo is damaged, stolen, destroyed, or lost during transit, the policy may help cover the financial loss depending on the cause of damage and policy wording.

For many businesses, cargo represents a significant financial investment. A shipment of electronics, equipment, inventory, machinery, or specialized products can be worth tens or even hundreds of thousands of dollars. Without cargo insurance, the financial impact of a loss may fall directly on the business.

Cargo insurance is commonly used by trucking companies, freight brokers, manufacturers, wholesalers, importers, exporters, distributors, and logistics providers that move products regularly throughout Ontario and beyond.

What Type of Insurance Covers Cargo?

There is no single cargo policy that fits every transportation operation. The type of insurance required often depends on who owns the goods, who transports them, and how the shipment moves through the supply chain.

A trucking company may require motor truck cargo insurance because it physically transports cargo for customers. A manufacturer importing products from overseas may rely on marine cargo insurance. A freight broker arranging transportation through third-party carriers may consider contingent cargo insurance to help protect against coverage gaps.

Understanding which party is responsible for the cargo is often one of the most important parts of building the right insurance program.

Motor Truck Cargo Insurance Explained

Motor truck cargo insurance is one of the most common forms of cargo coverage in Canada.

It is designed for trucking companies transporting goods owned by customers. Many shippers require proof of cargo insurance before awarding transportation contracts because they want confidence that their products are protected while moving through the supply chain.

Coverage may help respond to losses involving:

- Theft

- Fire

- Collision damage

- Overturn incidents

- Certain loading and unloading exposures

For example, a trucking company hauling building materials from Oakville to Ottawa may carry motor truck cargo insurance to help protect customer goods throughout transit.

How Does Marine Cargo Insurance Work?

Despite the name, marine cargo insurance is not limited to ocean transportation.

Modern marine cargo insurance often follows cargo through several stages of transportation, including truck, rail, air freight, and ocean freight. The purpose is to protect the goods as they move through the supply chain rather than focusing on a single transportation method.

This makes marine cargo insurance particularly useful for importers, exporters, wholesalers, and manufacturers whose products may travel through multiple carriers before reaching their final destination.

Many Ontario businesses rely on marine cargo insurance because their inventory often moves across provincial, national, or international borders before reaching customers.

Get a quote to review marine cargo insurance options based on your shipping routes and cargo values.

What Is Contingent Cargo Insurance?

Contingent cargo insurance is commonly associated with freight brokers.

Unlike trucking companies, freight brokers usually arrange transportation rather than physically moving cargo themselves. Because of this, brokers often rely on a motor carrier’s cargo insurance as the primary layer of protection.

Contingent cargo insurance may provide additional protection if:

- A carrier’s policy is insufficient

- Coverage is denied

- The carrier’s insurance has expired

- Certain exclusions apply

For freight brokers managing shipments throughout Ontario and North America, contingent cargo insurance can be an important part of managing contractual risk.

Common Cargo Insurance Risk Factors

The cost and structure of cargo insurance often depend on what is being shipped, where it moves, and how exposed the goods are during transit.

Higher shipment values usually require higher limits.

Electronics, pharmaceuticals, and high-value goods may increase risk.

Longer routes and cross-border shipments can affect underwriting.

Past cargo losses may influence pricing and coverage terms.

What Cargo Insurance Can Cover

Cargo insurance coverage depends on the insurer and policy wording, but it is commonly designed to protect against losses such as:

- Theft

- Fire

- Collision damage

- Overturn incidents

- Vandalism

- Certain weather-related events

- Loading or unloading damage

The type of cargo being transported also matters. Electronics, pharmaceuticals, refrigerated products, high-value machinery, and hazardous materials often require specialized underwriting because they present different levels of risk.

Coverage should always reflect the actual cargo being transported rather than relying on generic limits.

What Is Not Covered by Cargo Insurance?

One of the most common questions businesses ask is not what cargo insurance covers, but what it does not cover.

Coverage depends on the policy wording, insurer, cargo type, and cause of loss. While cargo insurance is designed to protect goods during transit, certain situations may be excluded or limited.

Common exclusions may include:

- Improper packaging

- Wear and tear

- Gradual deterioration

- Certain delays with no physical damage

- Intentional acts

- Losses outside the policy territory

This is why cargo insurance should be reviewed alongside transportation contracts and shipping procedures. A business shipping electronics will often have different insurance needs than one transporting building materials or consumer products.

Get a quote to review cargo insurance coverage and understand how policy exclusions may apply to your operations.

How Much Is Cargo Insurance?

Cargo insurance costs vary significantly depending on the operation, cargo value, transportation routes, and overall exposure.

Approximate annual ranges may include:

- Small trucking operations: approximately $1,500 to $5,000+

- Mid-sized fleets: approximately $5,000 to $20,000+

- Freight brokers with contingent cargo coverage: approximately $1,000 to $10,000+

- Importers and exporters: highly variable based on shipment volume and cargo values

Factors affecting cost include:

- Cargo value

- Cargo type

- Claims history

- Shipping territory

- Theft exposure

- Annual revenue

- Coverage limits selected

A fleet hauling electronics may face different underwriting considerations than one transporting building materials because the cargo value and theft exposure are often substantially different.

Ontario Cargo Insurance Coverage Comparison

Different types of cargo insurance serve different roles in the supply chain. Understanding who is responsible for the cargo can help determine which coverage may be appropriate.

| Coverage Type | Who Typically Uses It | Primary Purpose |

|---|---|---|

| Motor Truck Cargo Insurance | Trucking Companies | Protects customer goods while being transported by truck. |

| Marine Cargo Insurance | Importers, Exporters, Manufacturers | Protects cargo moving through truck, rail, air, and ocean transit. |

| Contingent Cargo Insurance | Freight Brokers | Provides additional protection if a carrier's cargo policy fails to respond. |

Why Cargo Values Matter for Insurance

Many businesses purchase cargo insurance when they first begin shipping products and then rarely review their limits.

As operations grow, shipment values often increase significantly. A company that once shipped $25,000 worth of inventory may eventually be shipping $150,000 or more in a single load. If coverage limits have not been updated, a large loss could leave part of the shipment uninsured.

Businesses should periodically review:

- Average shipment value

- Maximum shipment value

- Seasonal inventory increases

- International shipping exposure

- High-value products

Cargo insurance should reflect the actual value of goods moving through the supply chain today, not what the business shipped several years ago.

Case Study: Cargo Insurance Claim Example

A real Ontario cargo theft case shows how freight losses can affect shippers, carriers, and logistics businesses. In 2025, Peel Regional Police investigated a trailer and freight theft case involving stolen cargo reportedly valued at more than $1.5 million.

According to CityNews Toronto’s report on the Brampton trailer and freight theft case, multiple victims reported trailers loaded with freight being stolen after arranging transportation services. The case was also covered by TruckNews’ report on the $1.5 million freight theft investigation.

While public reports do not confirm the final insurance claim outcomes, the case highlights why cargo insurance can matter for Ontario businesses. Theft, fraud, misdirected freight, and transportation interruptions can create serious financial losses before goods ever reach the customer.

Get a quote to review cargo insurance options for your shipments, freight operations, or logistics business.

Common Cargo Insurance Mistakes

Many businesses assume another party’s insurance will always protect their cargo. That assumption can create problems when a carrier’s coverage is limited, denied, expired, or does not reflect the full shipment value.

Other common mistakes include:

- Underestimating cargo values

- Not reviewing policy exclusions

- Assuming marine cargo only applies to ocean freight

- Failing to verify carrier insurance

- Overlooking contingent cargo coverage

- Not updating limits as shipment volumes increase

Cargo insurance should be reviewed whenever shipment values, routes, carriers, or transportation methods change significantly.

Why Work With James Inwood

Cargo insurance can be more complex than many businesses expect because multiple parties may be involved in a shipment. Freight brokers, trucking companies, importers, exporters, cargo owners, and logistics providers may all have different responsibilities and insurance requirements.

James Inwood works with transportation companies, freight brokers, logistics providers, manufacturers, distributors, and commercial businesses across Ontario, including Oakville and the Greater Toronto Area. He helps businesses structure cargo insurance around their actual transportation operations and contractual obligations.

Get a quote or book a meeting with James Inwood to review cargo insurance options for your transportation or logistics business.

Frequently Asked Questions

Cargo insurance is designed to protect the value of the cargo itself, while carrier liability insurance is based on the transportation company’s legal responsibility for a loss. A carrier may not always be responsible for the full value of damaged goods, which is why many businesses purchase separate cargo insurance to protect their financial interest in the shipment.

Freight brokers often consider contingent cargo insurance because they rely on third-party carriers to move shipments. If a carrier’s cargo insurance does not respond to a loss or the available coverage is insufficient, contingent cargo insurance may provide an additional layer of protection depending on the policy wording.

Marine cargo insurance can apply to cargo moving by truck, rail, air, and ocean transportation. The name comes from the historical origins of cargo insurance, but modern marine cargo policies are often designed to follow goods through multiple stages of transportation.

High-value electronics, pharmaceuticals, alcohol, tobacco products, refrigerated goods, and hazardous materials often require additional underwriting. These cargo types may present higher theft exposure, spoilage risks, regulatory requirements, or specialized transportation concerns that can affect coverage and pricing.

Cargo insurance limits should be reviewed whenever shipment values, transportation routes, cargo types, or business operations change significantly. Many growing businesses discover that their original coverage limits no longer reflect the true value of goods moving through their supply chain.

James Inwood is an Ontario-based insurance broker who works with trucking companies, freight brokers, logistics providers, manufacturers, distributors, and commercial businesses throughout Ontario. He helps businesses understand cargo insurance, transportation liability, marine cargo coverage, contingent cargo insurance, and how commercial insurance policies respond when goods are moving through the supply chain. His approach focuses on practical risk management that aligns insurance coverage with real business operations.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn