Small Business Insurance in Oakville

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Small Business Insurance in Oakville

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Running a small business in Oakville comes with risk, even when the business itself seems straightforward. A customer injury, property damage claim, equipment loss, lawsuit, cyber issue, or employee benefit concern can affect operations quickly.

Small business insurance is designed to help protect the business financially when unexpected problems happen. The right coverage depends on what the business does, how many employees it has, whether clients visit the property, and how much risk the operation creates.

At a Glance: Small Business Insurance

- Small business insurance helps protect against financial loss

- General liability insurance is one of the most common coverages

- Commercial property insurance protects business assets

- Group insurance can help support employees

- Insurance costs depend on business type and exposure

- Contractors, retail businesses, consultants, and offices all have different risks

- Some clients, landlords, or lenders may require proof of insurance

- Coverage can often be customized for small businesses

What Is Small Business Insurance?

Small business insurance is a broad term used for different types of commercial insurance designed for business operations. Instead of one single policy, small business insurance is often a combination of coverages that work together.

This may include:

- General liability insurance

- Commercial property insurance

- Professional liability insurance

- Commercial auto insurance

- Cyber insurance

- Business interruption insurance

- Group insurance for employees

The structure depends on the type of business and the risks involved.

What Is Liability Insurance for Small Business?

General liability insurance for small business helps protect against claims involving bodily injury, property damage, or legal liability connected to business operations.

Examples may include:

- A customer slipping inside a retail store

- Property damage caused during contractor work

- A client injury at an office

- Damage caused while working at a customer site

General liability insurance is one of the most common starting points for small business coverage in Ontario.

Many landlords, commercial leases, contractors, and vendor agreements may require proof of liability insurance before work begins.

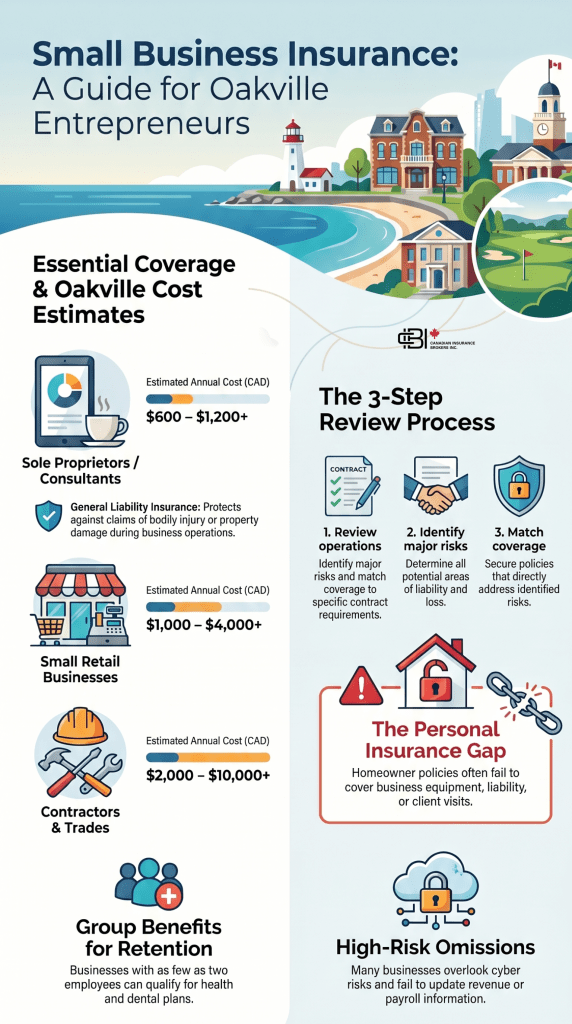

Group Insurance for Small Business

Group insurance helps businesses provide health and dental benefits to employees.

Small businesses in Oakville may use group insurance to help with:

- Employee retention

- Recruitment

- Extended health coverage

- Dental coverage

- Prescription drug coverage

- Disability coverage

- Life insurance benefits

Even businesses with only a few employees may qualify for group insurance plans. Professional offices and growing businesses often use group benefits as part of employee compensation packages.

Small Business Loan Insurance

Some lenders may require insurance when financing commercial property, equipment, or business loans.

Depending on the situation, this may involve:

- Property insurance

- Key person insurance

- Life insurance connected to financing

- Business interruption coverage

Insurance requirements often depend on the lender, loan size, and business structure.

Most Common Small Business Insurance Coverages

Different businesses require different types of protection depending on their operations, employees, clients, and property exposure.

General Liability

- Customer injury claims

- Property damage claims

- Legal defense costs

Commercial Property

- Business equipment

- Inventory protection

- Fire and theft exposure

Professional Liability

- Service-related claims

- Errors and omissions

- Financial loss allegations

Cyber Insurance

- Data breach response

- Cyber attack costs

- Client information exposure

Coverage depends on policy wording, insurer approval, business operations, and industry classification.

How to Get Insurance for Your Small Business

Getting insurance for a small business usually follows a few key steps:

- Review how the business operates, including the type of work performed, customer interaction, and daily business activities

- Estimate annual revenue, number of employees, and the value of equipment or inventory

- Identify major risks such as liability exposure, property damage, cyber risks, or commercial vehicle use

- Review contracts, leases, or client requirements that may require specific coverage limits

- Compare insurance options based on the business type and level of exposure

- Adjust coverage as the business grows, hires employees, or takes on larger contracts

The process often involves reviewing risks first, then matching coverage to the business exposure.

Where to Get Small Business Insurance

Small business insurance can be arranged through commercial insurance brokers or insurers that specialize in business coverage.

Working with a broker can help compare:

- Coverage options

- Liability limits

- Industry-specific risks

- Pricing structures

- Policy exclusions

- Commercial insurer requirements

The goal is usually not just finding the lowest price, but understanding how the policy would respond during an actual claim.

Get a quote to compare small business insurance options based on your industry, operations, and coverage needs.

Why Small Businesses Often Underestimate Insurance Risk

Many small business owners assume insurance is mainly for large corporations or high-risk industries. In reality, smaller businesses are often more financially vulnerable when claims happen because they have fewer resources to absorb unexpected losses.

A single lawsuit, equipment theft, water damage claim, or cyber issue can interrupt operations quickly. Even businesses that seem low-risk, such as consultants, marketing agencies, or professional offices, can still face legal costs, client disputes, or liability exposure.

This is especially common for growing businesses that move from home-based operations into commercial spaces, hire employees, or begin signing larger contracts. Insurance usually becomes more important as the business becomes more visible and takes on greater responsibility.

Average Cost of Small Business Insurance in Oakville

Average costs vary widely depending on the business type.

Approximate Oakville ranges may include:

- Sole proprietors or consultants: approximately $600 to $1,200+ annually

- Small retail businesses: approximately $1,000 to $4,000+ annually

- Contractors and trades: approximately $2,000 to $10,000+ annually

- Restaurants or hospitality businesses: potentially higher

Businesses with physical storefronts, employees, vehicles, or higher customer traffic typically carry more exposure.

What Can Increase Small Business Insurance Costs?

Insurance pricing depends on insurer underwriting, industry type, business operations, and policy structure.

Common Small Business Insurance Mistakes

Many small businesses wait too long before reviewing insurance exposure. Common issues include:

- Assuming personal insurance covers business activities

- Underestimating liability exposure

- Not updating revenue or payroll information

- Overlooking cyber risks

- Not reviewing contractor certificates

- Choosing coverage based only on price

- Waiting until a claim occurs

Small businesses often evolve quickly, which means insurance should evolve as well.

Case Study: Film.Ca Cinemas Arson

An Oakville example shows why small business insurance can matter. In September 2025, Film.Ca Cinemas in Oakville was targeted in an attempted arson attack while the theatre was closed. The business reported damage to the entrance, but no staff or guests were injured.

You can read more in the Film.Ca Cinemas press release and the CityNews Toronto article on the Oakville cinema arson case.

For small business owners, this type of case highlights why coverage such as commercial property insurance, business interruption insurance, crime or vandalism coverage, and liability protection may be worth reviewing. A single incident can create repair costs, security concerns, temporary disruption, and financial pressure, even when no one is injured.

Why Work With James Inwood

Small business insurance is not just about meeting a requirement. The structure of the coverage affects how the business responds when claims, lawsuits, property damage, or operational interruptions happen.

James Inwood works with contractors, consultants, retail businesses, offices, and small business owners in Oakville, including Bronte, Glen Abbey, Kerr Village, Downtown Oakville, West Oakville, and Trafalgar. He also serves businesses across Ontario looking for commercial insurance guidance.

Get a quote or book a meeting with James Inwood to review insurance options for your small business.

Frequently Asked Questions

General liability insurance is not legally required for every small business in Ontario, but many landlords, clients, commercial leases, and vendor agreements may require proof of coverage before work begins. For example, contractors, retail stores, and service providers are often asked to carry at least $2 million in liability coverage before signing agreements or entering job sites.

Yes. A personal homeowner policy may not fully cover business activities, client visits, business equipment, or liability related to professional services. For example, a consultant working from home in Glen Abbey or a home-based online retailer in West Oakville may still need commercial coverage depending on the type of work and customer exposure.

Some business insurance policies can include crime coverage or employee dishonesty coverage, but this is usually added separately rather than included automatically under general liability insurance. Coverage may help protect against financial loss caused by theft, fraud, or misuse of business funds by employees, depending on the policy wording and limits selected.

Yes. Many insurers in Ontario offer group benefit plans for businesses with only a small number of employees. Even businesses with two to five employees may qualify for health, dental, disability, and life insurance benefits. Small businesses in Downtown Oakville and Trafalgar often use group benefits to help attract and retain employees.

Small businesses should usually review insurance coverage at least once per year or whenever operations change significantly. This can include hiring employees, purchasing equipment, moving locations, increasing revenue, signing larger contracts, or adding new services. Businesses often outgrow their original coverage faster than expected.

James Inwood is an Ontario-based insurance broker who works with consultants, retail businesses, offices, and commercial property owners across Oakville and Ontario. He helps small business owners understand how insurance applies in real operating situations, including liability exposure, property risk, employee benefits, contractor requirements, and commercial growth.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn