Startup Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Startup Insurance in Ontario

We provide professional insurance guidance for businesses and individuals through a secure and confidential quote process designed to be clear, efficient, and easy to begin.

Locally established in Oakville, Ontario

Coverage designed to match your business needs

Insurance options reviewed across markets and emailed to you

Starting a business is often framed around growth, funding and product development. Insurance usually shows up later, if at all. That tends to work until the moment something goes wrong.

In Ontario, startups operate in a fast-moving environment. Early-stage companies often have evolving services, informal processes, and limited resources. That combination creates risk that is not always obvious at the beginning.

Startup insurance is not about covering everything on day one. It is about understanding where exposure actually exists and making sure the business can absorb it.

At a Glance: Startup Insurance

- Most startups need liability coverage early

- Professional liability is critical for service and tech businesses

- Insurance is often required by contracts before revenue scales

- Costs are usually lower than founders expect

- Coverage should evolve as the business grows

What Startup Insurance Actually Means

Startup insurance is not a single policy. It is a group of coverages designed to protect a business from financial loss tied to its operations, services, or decisions. At a practical level, insurance addresses three types of risk:

- Claims from clients or third parties

- Financial loss tied to your work or advice

- Damage to business assets or interruption

For most startups, the primary exposure is not physical. It is financial. That is why liability coverage usually becomes relevant first.

Where Risk Starts for Startups

Risk does not begin when a company becomes “large.” It begins as soon as the business interacts with clients, users, or the public. Common early-stage exposures include:

- Delivering work that a client relies on

- Signing agreements that include liability clauses

- Handling customer data or sensitive information

- Operating without clearly defined scope or expectations

Even without significant revenue, these situations can lead to claims.

What Insurance Does a Startup Actually Need?

Most startups do not need every type of insurance immediately. Although there are a few core coverages that tend to come up early.

General Liability Insurance

General liability covers third-party claims for injury or property damage. It is often required when working with clients, landlords, or shared spaces.

Professional Liability (Errors and Omissions)

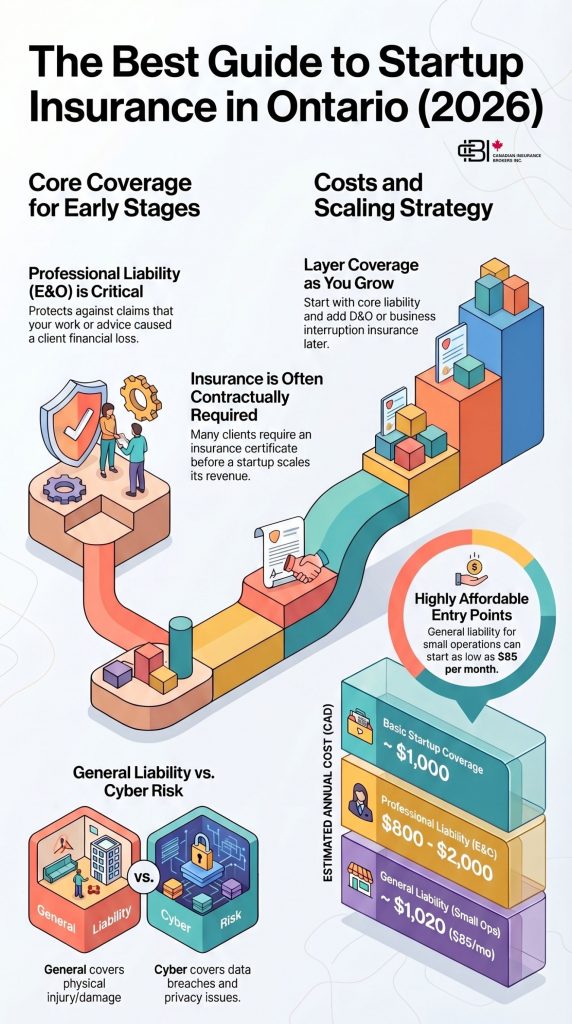

Professional liability, also called E&O insurance, protects against claims that your work or advice caused financial loss.

This is especially important for:

- Consultants

- Tech startups

- Agencies

- Service-based businesses

Cyber Liability Insurance

If your startup handles data, even at a small scale, cyber risk becomes relevant. Data breaches, privacy issues, and system failures are increasingly common.

Property and Equipment Coverage

Even lean startups rely on equipment. Laptops, servers, and tools represent real value and may not be covered under personal policies.

Additional Coverage as You Grow

As the business expands, additional coverage may include:

- Directors and officers (D&O) insurance

- Business interruption insurance

- Commercial auto (if applicable)

Most startups layer coverage over time rather than all at once.

What Startup Insurance Covers in Ontario

Startup insurance in Ontario is usually built around liability, financial risk, cyber exposure, and protection for business equipment. Most founders start with core coverage and expand it as the business grows.

Professional Liability

Protects against claims that your work or advice caused financial loss

- Client alleges your work caused a loss

- Important for consultants, agencies, and tech startups

- Legal defence costs can be significant

General Liability

Covers third-party injury or property damage claims

- Slip-and-fall or visitor injury claims

- Damage to client or landlord property

- Often required by contracts or leases

Cyber Liability

Helps with data breaches, privacy issues, and system disruption

- Customer data exposure

- Privacy-related incidents

- System interruption and response costs

Property and Equipment Coverage

Protects business tools, laptops, and other physical assets

- Damaged laptops or office equipment

- Theft of business property

- Useful even for lean operations

| Coverage Type | What It Helps Cover | Best For | Main Reason |

|---|---|---|---|

| Professional liability | Claims that your work caused client financial loss | Consultants, agencies, SaaS, service businesses | Work product and advice can create exposure early |

| General liability | Third-party injury or property damage | Any startup with clients, meetings, or leased space | Often required by contracts, landlords, or shared spaces |

| Cyber liability | Data breaches, privacy issues, and system failures | Tech startups and businesses handling data | Digital risk grows quickly even at a small scale |

| Property coverage | Laptops, tools, and equipment damage or theft | Startups with valuable physical business assets | Personal policies may not cover business property |

| D&O insurance | Claims against directors and officers | Funded startups or companies with boards | Governance risk grows as the business scales |

| Business interruption | Loss of income after a covered disruption | Startups with ongoing operations and revenue dependence | Helps absorb the impact of operational downtime |

| Commercial auto | Vehicles used for business operations | Startups using cars for deliveries, visits, or transport | Personal auto insurance may not fit business use |

Coverage needs vary by industry, contracts, data exposure, and business stage. This chart shows how startup insurance is commonly structured for Ontario businesses.

Why Professional Liability Comes Up So Often

Professional liability is often the first meaningful exposure for startups.

If a client believes your work caused financial loss, the claim does not need to be valid to create cost. Legal defense alone can be significant.

General liability does not respond to this type of situation. That gap is where professional liability insurance becomes essential, especially for service-based and tech-driven startups.

Startup Insurance Cost Breakdown

Startup insurance in Ontario is usually more affordable than founders expect. Typical ranges:

- Basic coverage: about $1,000 per year

- Professional liability: roughly $800 to $2,000 annually

- General liability: around $85 per month for small operations

Costs depend on industry, revenue, contracts and risk exposure.

The key takeaway is simple. Insurance is usually not the largest expense. The risk of not having it often is.

Small Business vs Startup Insurance

Startup insurance is often grouped with small business insurance, but the way it is used is different. Startups tend to:

- Change quickly

- Expand services

- Take on new types of risk early

This means coverage needs to be reviewed more often. A policy that fits today may not fit six months from now.

Flexibility matters more than completeness at the beginning.

How to Choose Startup Insurance Without Overcomplicating It

Choosing startup insurance does not need to be complicated. A practical approach is to focus on:

- Where your business creates risk for others

- What your contracts require

- How clients rely on your work

- What would create the largest financial impact

From there, coverage can be added as the business grows.

What Founders Often Miss

Many founders delay insurance because the business feels too small. In reality, exposure begins early. A client dispute, a missed expectation, or a data issue can happen at any stage.

The cost of responding to a claim, even if it does not lead to a payout, can be significant. Insurance is not just about paying claims. It is about handling the process around them.

How Insurance Changes as You Grow

Startup insurance is not static. As the business grows:

- Contracts become larger

- Insurance certificates (COI) are required

- Clients expect more formal coverage

- Data exposure increases

- Hiring introduces new risks

Coverage should evolve alongside the business. Regular review becomes part of operating responsibly.

Get a quote to align your startup insurance with your current stage and risk.

Visual: Finding the Best G2 Insurance in Ontario

Why Work With James Inwood

Startup insurance is often approached too late or treated too generally. Many founders either delay it or choose coverage that does not reflect how their business actually operates.

James Inwood works with startups across Ontario to identify where risk actually exists and build coverage that matches it. This includes reviewing contracts, understanding liability exposure, and helping coverage evolve as the business grows.

Get a quote or book a call with James Inwood to review your startup insurance.

Frequently Asked Questions

Not always, but once you begin working with clients or signing agreements, insurance becomes relevant quickly. Your end customers may ask for an insurance certificate, we can provide you with the right coverage and a certificate right away.

For most, professional liability is the first critical coverage, especially if your work impacts client outcomes. Depending on the location and other factors CGL Commercial General Liability should be considered.

Generally no. Basic coverage is relatively affordable compared to the potential financial exposure. Coverage can start as low as $80 per month and range depending on the business size and operations.

Yes. Most startups begin with core liability coverage and expand as the business grows. This often starts with a certificate request or a call with an insurance broker based on budget and scope.

James Inwood is an Ontario-based insurance broker who works with startups, consultants, and growing businesses.

He focuses on helping founders understand how insurance actually works in real scenarios, where risk begins, and how coverage should evolve as the business grows.

His approach is practical and advisory, helping businesses avoid gaps before they become costly problems.

James Inwood, Insurance Broker

RIBO licensed | LinkedIn